Will Innovative New Financial Regulator Be Hobbled Before It Even Starts?

by Lois Beckett ProPublica

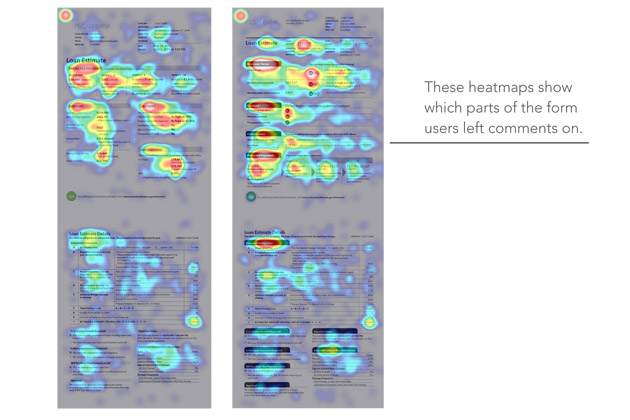

Want to know what people find most confusing about mortgage disclosure documents? Then check out these heat maps created by a new government regulatory agency.

The heat maps show two model mortgage forms that the agency posted on its website [1]. Users left more than 13,000 comments on the documents, and the maps show which parts of the form generated the most comments2014which may indicate, among other things, which parts are the most difficult to understand.

This more inclusive approach to regulation is one of the hallmarks of the new Consumer Financial Protection Bureau [2], a politically contentious agency that will open for business this Thursday.

The agency is trying to draw in consumers, since one of its jobs is to make sure that consumers understand the financial deals they’re making. It has a candy-colored website [2] that looks more like a social media start-up than a cluttered .gov page. It turned to Twitter [3] for a pre-launch “Open for Suggestions” campaign and then posted response videos [2] on its YouTube page [4].

“Its openness thus far suggests the tantalizing possibility that it could be the nation’s first open-source regulator,” New York Times personal finance columnist Ron Lieber wrote last week [5].

Created as a result of last year’s financial reform law, the agency is supposed to be a “cop on the beat” overseeing consumer financial products such as mortgages, credit cards and payday loans.

But just how effective the bureau will be is still in question, in large part because of a partisan battle on Capitol Hill over how much power the agency should have to police banks and other financial institutions.

As part of a wider attack on last year’s Dodd-Frank legislation [6], a group of Republican legislators have promised to block the bureau from operating fully unless its ability to police businesses is put under bipartisan control.

Republicans want to replace [7] the bureau’s director2014nominated by the president2014with a five-member bipartisan board. They also want to make it easier for the bureau’s rules to be overturned, while some are also demanding that Congress be given control over the bureau’s budget.

Republicans have promised to filibuster the appointment of the bureau’s director (the nominee is former Ohio attorney general, and Jeopardy star, Richard Cordray [8]) until their demands are met.

Like many other news outlets, the financial news service Bloomberg lambasted the changes in an editorial [9] on Tuesday, saying it would politicize the agency and make it slower.

The bureau “was designed to move quickly (like the Federal Deposit Insurance Corp.) and not ploddingly (like the SEC, where three commissioners must pre-approve nearly everything the agency does),” Bloomberg opined.

At the moment, the bureau gets its funding from the Federal Reserve. This is a good thing, Bloomberg concluded, because it means the bureau is “insulated from the partisan funding fights that have hamstrung the SEC, the Commodity Futures Trading Commission and other regulators.”

It’s worth noting that the SEC, whose job to investigate and prosecute companies for financial fraud was expanded under Dodd-Frank, recently had its budget cut by $222.5 million [10] by the Republican-controlled House appropriations committee.

The bureau’s opponents aren’t backing down. Forty-four Republican senators have signed a letter vowing to oppose [11] the confirmation of any agency chief until the new regulator is restructured. On Tuesday, a key Republican senator described Cordrary, the current nominee, as “dead on arrival [8].” President Obama could bypass this issue by pushing the director through in a recess appointment [12]. (The Senate’s current recess is on hold due to debt ceiling negotiations [13].)

Until the bureau has a confirmed director, its regulatory powers are limited in significant ways [14]. As the Los Angeles Times has noted [15]:

The agency won’t have power, for instance, to crack down on mortgage brokers, some of which helped lead the nation into the housing debacle four years ago. It also won’t have authority over other largely unregulated sectors of the financial services industry, such as payday lenders and remittance companies such as Western Union, that it was created to police.

But as the political battle rages on and media scrutiny focuses on Elizabeth Warren’s political future [16], little attention has been given to what the bureau has actually done. And its initial efforts are interesting, especially because they show a commitment to open government [17] and real public engagement. (Ron Lieber noted [18] that its blog actually accepts comments2014″unlike, say, the White House’s.”)

The bureau’s mission is to create transparency in an industry dominated by confusing claims and mouse print [19]. Good design isn’t just a perk here2014it’s fundamental to the bureau’s regulatory efforts.

Case in point: One of the CFPB’s top priorities has been streamlining [1] the federally required mortgage disclosure documents. If that sounds like a mouthful, it’s worse on paper: two separate, complicated forms that are confusing for customers and, the bureau contends [20], also burdensome for many mortgage servicers to fill out.

The goal is to replace them with a single, two-page document that clearly answers the questions: “Can I afford this mortgage?” and “Can I get a better deal somewhere else?”

Two of the potential designs [21] for the new form [22] each have a note at the top, in bold print: “You have no obligation to choose this loan. Shop around to find the best loan for you.”

The bureau’s other projects [20] include improving transparency about credit card prices and fees, the exchange rates used for remittance transfers of money to other countries and the credit scores sold to consumers and creditors.

It’s worth noting that, while the financial industry has lobbied heavily against the bureau [23], its efforts may actually help businesses in the long run.

In a recent letter [24] to shareholders JP Morgan Chase’s chief executive, Jamie Dimon [25], noted that the company does not oppose the bureau. “If the CFPB does its job well, the agency will benefit American consumers and the system,” Dimon told shareholders. “Strong regulatory standards, adequate review of new products and transparency to consumers all are good things.”

New Yorker financial columnist James Surowiecki [26] has argued that the financial industry should see the creation of a bureau as a boon, not a threat [27]. “Meatpackers hated the Meat Inspection Act of 1906, but it rescued the industry from the aftereffects of the publication of 2018The Jungle,’ ” Surowiecki wrote. “At a time when Americans profoundly distrust the financial industry … [the CFPB] could turn out to be the friend banks never knew they needed.”

~

4closureFraud.org

I have been dealing with these illegal bank promissory notes and mortgages notes for almost 12 years now and it is so easy for me to spot the fraud in the factum ~ constructive fraud ~ forgeries ~ etc

Give me any of the contract forms used by the banks that are approved by the Fed Res and Fannie Mae and I will point-out to anyone from the lowest one with 24 violations to Bank of Am’s with 31 violations of contract law…..

The constructive fraud element is where the had full and prior knowledge of this fraud when these contracts were drafted to be used by millions of loan originators [most of the lower levels did have a clue, just doing what they were told to do] but the really criminal part is when they get the consumer to agree to these terms [which many attorneys cannot decode] so you become a party to these crimes yourself???

Kinda like the credit card agreements which are totally “QUASI COMTRACTS” [meaning take it or leave it] and Congress allows the cc companies to continue to use these documents that are enudated with fraud and violations of contract law??

If the banking regulators [what a crook] the attorney generals, the banksters attorneys, the judges or any juror [if you are lucky enough to have requested one] cannot find anything wrong with these promissory or mortgage notes, then send them to me and I will hi-lite them at no fee……….lol

The 100 year old web of deceipt. theft and extortion has made the Rothschild Dynasty rich beyond any mathematical measures, as well as, all of the other crooks that have been and are now involved…

The Bible states that there will at a time so needed that it will be called the Day of Jubilee when all encroached and stolen lands will be returned to the rightful owners………..

Jim, what about the bundling of too many UNSECURED bad loans with a fraction of good loans which caused all of the loans in that pool to fail. That is where the proof of intent to harm is. They hid that GIANT RISK and packaged those up and sold those as AAA rated. THE LIARS LOANS are also proof of intent to cause harm. The people did not approve their own loans. It was up to the bank to investigate. When I bought my house in 1992, it took 4 months to get a mortgage approved with A+ credit and $100,000 dollars down on a $290,000.00 home. When we re-fied in 2007 it took 2 weeks to get approved though we still fully qualified for the re-fi but I knew the house value appraisal was way to high and the comps they used did not even come close to our house..Not one house they comped with ours was valued anywhere near what our house appraised out at. What we did not know was they were doing a PONZI SCHEME with home “loans” but the average person could have never known this though there were warning signs we trusted too much and had no reason not to..There were no protections for consumers and the “lenders” used the weapon of gaining our trust to deceive us.

If I did question the appraisal would that have made a difference? My question is what were the quality of the loans in the loan pool they put us in and how many of those loans were too risky and failed? They created the bubble, caused the bubble to burst and it was intentional. We knew they would possible sell our “loan” off to a second lender but we did not know about the bundling of the loans. That was the biggest crime here. I would have never agreed to that, not for one minute. The credit default swap insurance they aquired is the proof they knew what they were doing was incredibly risky.

YES MADE TO SOUND LIKE 3 YR OLD BECA– USE THAT IS HOW THEY ALL MAKE ME FEEL. WE CANT DO THIS WE CANT DO THAT SO WHY be?????????????????????????? AT ALL. WE STILL NOT GET HELP. ALOT OF OUR TROUBLES TARTED WITH THE MORTGAGE BROKERS….HELLO mcfly. IF THE WELLS FARGO MORGTAGE BROKERS LIED ON MORTGAE APPLICATIONS FOR SSUBPRIME MORTGGES WHAT DO YOU THINK THEY DID ON CONVENTIONAL MORTGAGES. TOLD THE TRUTH????? ONE PERSON WORKING, SPO– USE UNEMPLOYED we should have been denied. that would have been ok it was 2006 there is something called renting. my husband got a job late on but my SALARY WAS NOT WHAT SHE QUOTED ON MY APPLICATION. AFTER GOING THROUGH MORTGAGE MODIFICATION HELL WITH WELLS FARGO THEN HAVING HAMP FILE MOVED AND MY PAPER WORK LOST LOOKED INTO WHY. AND FOUND ALL MY MORTGAGE PAPERS. THERE IT WAS ON THE BOTTOM OF THE STACK AND OF COURSE JUST LIKE ALL MY OTHER PEPERS UNSIGNED MY MORTGAGE APPLICATION. SHE ADDED ABOUT 700$ TO WHAT I COULD HAVE POSSIBLY MADE IN A WEEK. SEE IT WAS EASY FOR HER. I WAS OUT OF TOWN AND I WAS AN HOURLY EMPPLOYEE. FEW HOURS HERE A FEW HOURS THERE. I AM PN THE NOTE NOT MY HUSBAND. COULD NOT AFFORD THE HO– USE FROM THE SIGNING AND SHE NEW IT. WE STRUGGLED AND THIS IS THE OUTCOME WAITING FOR FORECLOSURE. SO NOT SURE HOW THEY THINK WELLS FARG IS IMMUNE TO THE OTHER LOANS THEY WROTE.

Mike; Thanks again for your steadfastnessand loyalty to truth. May your people rise up to appreciate what you are doing. That last download made me sick and I am glad for Bank of Italy. America. And. i hope Deutsche gets a fine of atlesast $300,000,,000 fdor starters.