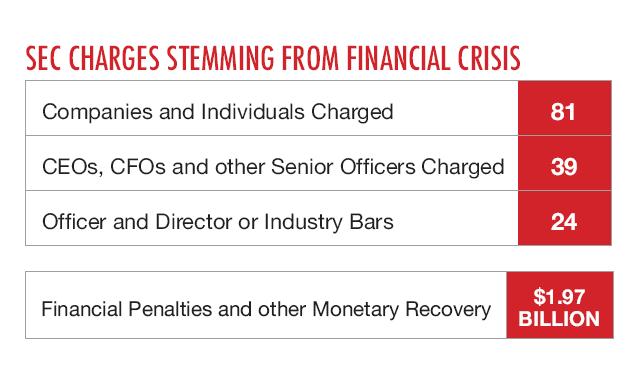

Notice how the above graphic does not include a section for PROSECUTIONS stemming from the financial crisis.

~

Citigroup to Pay $285 Million to Settle SEC Charges for Misleading Investors About CDO Tied to Housing Market

Former Citigroup Employee Separately Charged for His Role in Structuring Transaction

FOR IMMEDIATE RELEASE

2011-214

Washington, D.C., Oct. 19, 2011 – The Securities and Exchange Commission today charged Citigroup’s principal U.S. broker-dealer subsidiary with misleading investors about a $1 billion collateralized debt obligation (CDO) tied to the U.S. housing market in which Citigroup bet against investors as the housing market showed signs of distress. The CDO defaulted within months, leaving investors with losses while Citigroup made $160 million in fees and trading profits.

Additional Materials

- SEC Complaint Against Citigroup Global Markets Inc.

- SEC Complaint Against Brian H. Stoker

- Order in the Matter of Credit Suisse Alternative Capital, Credit Suisse Asset Management and Samir H. Bhatt

The SEC alleges that Citigroup Global Markets structured and marketed a CDO called Class V Funding III and exercised significant influence over the selection of $500 million of the assets included in the CDO portfolio. Citigroup then took a proprietary short position against those mortgage-related assets from which it would profit if the assets declined in value. Citigroup did not disclose to investors its role in the asset selection process or that it took a short position against the assets it helped select.

Citigroup has agreed to settle the SEC’s charges by paying a total of $285 million, which will be returned to investors.

The SEC also charged Brian Stoker, the Citigroup employee primarily responsible for structuring the CDO transaction. The agency brought separate settled charges against Credit Suisse’s asset management unit, which served as the collateral manager for the CDO transaction, as well as the Credit Suisse portfolio manager primarily responsible for the transaction, Samir H. Bhatt.

“The securities laws demand that investors receive more care and candor than Citigroup provided to these CDO investors,” said Robert Khuzami, Director of the SEC’s Division of Enforcement. “Investors were not informed that Citgroup had decided to bet against them and had helped choose the assets that would determine who won or lost.”

Kenneth R. Lench, Chief of the Structured and New Products Unit in the SEC Division of Enforcement, added, “As the collateral manager, Credit Suisse also was responsible for the disclosure failures and breached its fiduciary duty to investors when it allowed Citigroup to significantly influence the portfolio selection process.”

According to the SEC’s complaints filed in U.S. District Court for the Southern District of New York, personnel from Citigroup’s CDO trading and structuring desks had discussions around October 2006 about the possibility of establishing a short position in a specific group of assets by using credit default swaps (CDS) to buy protection on those assets from a CDO that Citigroup would structure and market. After discussions began with Credit Suisse Alternative Capital (CSAC) about acting as the collateral manager for a proposed CDO transaction, Stoker sent an e-mail to his supervisor. He wrote that he hoped the transaction would go forward and described it as the Citigroup trading desk head’s “prop trade (don’t tell CSAC). CSAC agreed to terms even though they don’t get to pick the assets.”

The SEC alleges that during the time when the transaction was being structured, CSAC allowed Citigroup to exercise significant influence over the selection of assets included in the Class V III portfolio. The transaction was marketed primarily through a pitch book and an offering circular for which Stoker was chiefly responsible. The pitch book and the offering circular were materially misleading because they failed to disclose that Citigroup had played a substantial role in selecting the assets and had taken a $500 million short position that was comprised of names it had been allowed to select. Citigroup did not short names that it had no role in selecting. Nothing in the disclosures put investors on notice that Citigroup had interests that were adverse to the interests of CDO investors.

According to the SEC’s complaints, the Class V III transaction closed on Feb. 28, 2007. One experienced CDO trader characterized the Class V III portfolio in an e-mail as “dogsh!t” and “possibly the best short EVER!” An experienced collateral manager commented that “the portfolio is horrible.” On Nov. 7, 2007, a credit rating agency downgraded every tranche of Class V III, and on Nov. 19, 2007, Class V III was declared to be in an Event of Default. The approximately 15 investors in the Class V III transaction lost virtually their entire investments while Citigroup received fees of approximately $34 million for structuring and marketing the transaction and additionally realized net profits of at least $126 million from its short position.

The SEC alleges that Citigroup and Stoker each violated Sections 17(a)(2) and (3) of the Securities Act of 1933. While the SEC’s litigation continues against Stoker, Citigroup has consented to settle the SEC’s charges without admitting or denying the SEC’s allegations. The settlement is subject to court approval. Citigroup consented to the entry of a final judgment that enjoins it from violating these provisions. The settlement requires Citigroup to pay $160 million in disgorgement plus $30 million in prejudgment interest and a $95 million penalty for a total of $285 million that will be returned to investors through a Fair Fund distribution. The settlement also requires remedial action by Citigroup in its review and approval of offerings of certain mortgage-related securities.

The SEC instituted related administrative proceedings against CSAC, its successor in interest Credit Suisse Asset Management (CSAM), and Bhatt. The SEC found that as a result of the roles that they played in the asset selection process and the preparation of the pitch book and the offering circular for the Class V III transaction, CSAM and CSAC violated Section 206(2) of the Investment Advisers Act of 1940 (Advisers Act) and Section 17(a)(2) of the Securities Act and that Bhatt violated Section 17(a)(2) of the Securities Act and caused the violations of Section 206(2) of the Advisers Act by CSAC.

Without admitting or denying the SEC’s findings, CSAM and CSAC consented to the issuance of an order directing each of them to cease and desist from committing or causing any violations, or future violations, of Section 206(2) of the Advisers Act and Section 17(a)(2) of the Securities Act and requiring them to pay disgorgement of $1 million in fees that it received from the Class V III transaction plus $250,000 in prejudgment interest, and requiring them to pay a penalty of $1.25 million. Without admitting or denying the SEC’s findings, Bhatt consented to the issuance of an order directing him to cease and desist from committing or causing any violations or future violations of Section 206(2) of the Advisers Act and Section 17(a)(2) of the Securities Act and suspending him from association with any investment adviser for a period of six months.

The SEC’s investigation was conducted by Andrew H. Feller and Thomas D. Silverstein of the Enforcement Division’s Structured and New Products Unit with assistance from Steven Rawlings, Brenda Chang and Elisabeth Goot of the New York Regional Office. The SEC trial attorney who will lead the litigation against Stoker is Jeffrey Infelise.

For more information about dozens of other SEC enforcement actions related to the financial crisis, visit the SEC website at: http://www.sec.gov/spotlight/enf-actions-fc.shtml.

# # #

For more information about these enforcement actions, contact:

Kenneth R. Lench

Chief of Structured and New Products Unit, SEC Division of Enforcement

(202) 551-4938

Reid A. Muoio

Deputy Chief of Structured and New Products Unit, SEC Division of Enforcement

(202) 551-4488

http://www.sec.gov/news/press/2011/2011-214.htm

~

4closureFraud.org

These continued slaps on the wrist are going to accomplish one thing –

Pouring more gasolne on the smoldering fury of wronged Americans.

“First we had the Community Reinvestment Act which made it mandatory for financial institutions to lend money into formerly “redlined neighborhoods”. ”

This lie won’t go away. Banks could no longer “deny” loans to other wise credit worthy individuals based on race or location. They were not “forced”. Once the goons at the Banks/Fannie et al gutted regulation, the CRA didn’t mean anything that it has intended to mean. Banksters were free to attack and draw all kinds of people around the bend and put them in loans they new well were designed to fail.

You’re absolutely correct. William Black, my hero, has covered this extensively. The real problem was Liar’s Loans which were never given to subprime, poor or disadvantaged customers. As Prof Black has pointed out, the name was given to these loans by the industry itself and was 100% accurate.

Caitlin……than how did 50 year old women……living by themselves, in low income neighborhoods, with nearly no income…..receive any home loans at all. Of course they were subprime and ALT-A loans and purposely designed to fail.

CAITLIN O…ABSOLUTELY CORRECT THAT THE INDUSTRY GAVE THE LIARS LOANS BUT, AS USUAL THE DEVIL IS IN THE DETAILS….READ THIS ARTICLE:

HOW THE U.S. GOVERNMENT ENGINEERED THE CURRENT ECONOMIC CRISIS:

http://techcrunch.com/2008/09/26/the-us-government-engineered-the-current-economic-crisis/

Nearly all of the politicans are traitors from the top down and on the inside… The change has to come through all of us, WE THE PEOPLE have to exert our Constitutional Rights and demand the changes…I refuse to vote for any of them from either commie party…they are all either hijacked by NWO corruption or members of the U.N./NEW WORLD ORDER……No one wants this Global Hitler Plan…so stop conforming and paying…We are allowing it by passively accepting everything they do to all of us and tell all of us to do…They raise taxes, take away more and more of our rights…and WE THE PEOPLE do nothing at all….the traitors are still all doing business as usual and robbing all of us to pay for all of their fraud on a daily basis….WAKE UP AMERICA…STOP CONFORMING TO IT AND STOP ALLOWING IT…!! If we keep allowing it, soon it will be all out GLOBAL TOTALITARIANISM……THE NWO is waiting to strike the final blow….to take over our NATIONAL SOVEREIGNTY….WE THE PEOPLE MUST THROW ALL OF THE TRAITOR POLITICIANS OUT AMERICA! WRITE IN YOUR CANDIDATE….ON PAPER BALLOTS…DEMAND WE THE PEOPLE COUNT OUR OWN VOTES..END THE ELECTORAL COLLEGE..IT IS A SHAM AND A FRAUD……DEMAND WE ARE ISSUED OUR OWN CURRENCY AS THE U.S CONSTITUTION REQUIRES..OPEN UP FORT KNOXX TO THE PEOPLE…HOLD THE U.S TREASURY ACCOUNTABLE FOR WHERE ARE THE ORIGINAL NOTES?….HOLD THE POLITICIANS ACCOUNTABLE FOR THE MORTGAGE FRAUD FROM PAST AND PRESENT ADMINISTRATION…WHY IS THE FED COLLECTING TRILLIONS A MONTH IN MORTGAGE MONEY AND BUYING U.S. TREASURIES WITH THAT MONEY? WHO ARE THEY SELLING THOSE TREASURIES TOO….? THEY ARE BACKED BY NO COLLATERAL AT ALL …THE FED IS BLOWING UP ANOTHER BUBBLE… …ABOLISH THE FED..REMOVE OURSELVES FROM THE U.N, NO MORE FEDERAL TAXES, THERE SHOULD BE A STATE BANK IN EACH STATE THAT COLLECTS OUR TAXES, WITH FULL ACCOUNTING BI YEARLY AND AUDITING YEARLY… THAT COLLECTS THE TAXES FOR THE STATES..AFTER THE BILLS ARE PAID, WITH FULL ACCOUNTING OF COURSE,.LET THE PEOPLE OF EACH STATE DECIDE AND VOTE ON HOW THAT MONEY IS ALLOCATED……..LET THE TBTF EAT THEIR FRAUD AND, FAIL…DEMAND CONGRESS RE-ESTABLISH THE U.S. CONSTITUTION TO ITS ORIGINAL FORM……OR WE ARE DOOMED….!!!

Watching HO– USE OF CARDS on CNBC..About the housing boom and what FANNIE/FREDDIE, WALL STREET AND THE RATINGS AGENCIES DID…AND WHAT THE FEDERAL REGULATORY AGENCIES DID NOT DO….TO STOP THEM…THEY DID NOTHING…AT ALL..Pretty interesting….There is no way this was not an evil Hitler Plan from the begining to bankrupt the 99%….by the NEW WORLD ORDER, IN COLLUSION WITH THE U.S. GOVERMENT…PURE EVIL…I WOULD NOT PAY ANY OF THE BASTARDS…AT ALL..!!

Rob – subprime mortgages were usually targeted at older, poorer people, and to people of color, sometimes through church communities. To me, the most tragic stories are those where people who already had high amounts of equity or even owned their homes outright were talked into ‘putting their equity to work’ by taking out subprime mortgages, even though some of them qualified for prime rates.

How did borrowers qualify? Fraudulently. Sometimes the mortgage broker changed the income reported by the borrower, sometimes the borrower was put into an ARM when they thought they were getting a fixed rate loan, often the value of the house was fraudulently inflated so the loan to value ratio would pass.

Mortgage brokers were motivated to sell subprime by earning better commissions than from prime because the interest rates earned by the banks were higher. No one cared whether the older, poorer person could pay the loan back because the lender wasn’t going to hold it, anyway, but just sold it on up the chain in the securitization process.

These loans had pretty much failed and passed out of the system by the middle to the end of 2009.

Since then, the failures have largely been among Alt-A loans. These were made to people with more means than subprime borrowers and involved larger amounts of money because the houses had higher prices. They were also called stated income or liar’s loans because the borrower didn’t have to document their income. In place of proof of income, lenders accepted high FICO scores – which pretty much eliminated most poorer borrowers. These were attractive to mortgage brokers because the commissions on higher value homes (i.e. bigger loans) were higher.

The million dollar question you’re correctly asking is “Why would any bank make a loan to anyone when simple logic says the loan is going to fail?”

And the answer is big money and low risk.

There was a ton of money made at every step of the origination and securitization process. Fees and commissions were earned at every level. No one cared or needed to care about the quality or risk of the loans because nobody held onto them long enough to get stuck with losses. Except for the securities investors of course, they cared deeply about the quality because they were the last stop on the line and they were the ones who were to hold onto the mortgage long term.

Investors had no interest in buying mortgages that were doomed to fail so investment banks got around that one by lying. Goldman, Merrill and the other mafia dons paid the rating agencies for AAA ratings, sold trillions of dollars worth of toxic mortgages to towns, little banks, firemen pension funds etc. and then turned around and shorted their own securities, ensuring that they would make money when the mortgages failed, as they were practically guaranteed to do.

It was a process steeped in fraud and corruption at every step. Through a modern day Gresham’s dynamic, honest players were driven out of business by the corrupt. After destroying economies around the world, it will probably end up bringing down governments as people respond with increasing outrage to the destruction of their livelihoods, communities and futures while watching the rich get richer and the criminals escape justice with impunity.

Really, Rob, it was just greed, enabled by deregulation and the systematic defanging of the few remaining regulators. Just greed. Not a new world order, not the ‘other’, not the CRA which was passed under Carter and never caused anything even approaching a crisis in 30 years. It’s a classic example of the banality of evil.

It truly infuriates me, shames me and, at the same time, breaks my heart to think that our great country could have created this fiasco and could have exported it around the world.

BOTTOM LINE…WE WERE ALL SET UP TO FAIL…THE ENTIRE COUNTRY….AN ATTORNEY TOLD ME THAT THE GOVERNMENT IS GOING TO TAKE EVERY HO– USE BACK FROM EVERY SINGLE ONE OF US…I SAID, THAT IS COMMUNISM…THE ATTORNEY SAID, THAT IS TOTAL COMMUNISM….HE SAID…HE DOES NOT WANT TO BE HERE TO SEE THIS, HE IS GOING TO LEAVE THE COUNTRY BECA– USE IF THE ECONOMY GETS ANY WORSE….IT WONT MATTER IF YOUR PAYING YOUR MORTGAGE OR NOT IT WILL BE ANARCHY……CNBC REPORTED THAT THE FEDERAL GOVERNMENT WANTS TO BE THE BIGGEST LANDLORD IN THE WORLD…..VIA FANNIE AND FREDDIE…I SAY…FUCK THEM….!!!!

Like my friend who has 3 years left to pay on her house…lost her job in bank security of 20 years and her husband is a carpenter who has not had steady work since the bubble burst….Chase has already had some asshole out to her house to take pix of her house…she is three mos. behind….THIS WAS A HITLER PLAN…PERIOD…FICO SCORES, LIARS LOANS…TILA VIOLATIONS…ALL PART OF THE SET UP TO FAIL…ALONG WITH STRATEGIC NEITSZCHE CLASSWARFARE TACTICS BY THE NAZIS AT THE FED AND THE TREAS…..TO TRY AND FORCE ALL OF US TO PAY FOR WALL STREETS FRAUD..AND STEAL EVERYTHING FROM ALL OF US, INCLUDING OUR COUNTRY…..CRIMINALS AND TREASONISTS ALL OF THEM…..!! LOCK EM UP AND THROW OUT ALL OF THE TRAITOR POLITICIANS….ASAP!!!!

NOT A NEW WORLD ORDER?????….FOR THE LOVE OF GOD CAITLIN WAKE UP…BEFORE THEY LOAD YOU ON THE TRAIN TO THE FEMA CAMP…..

That fine represents the value of about 600 homes, I call this chum change or gas money.

“What do you do when you find out your heroes are assholes? One of the most difficult parts of discovering the truth of MERS and mortgage securitization is that the curtain of fantasy is stripped away leaving quite a bit of heartache as you realize the heroes, the ones you look to as paragons of virtue are in it for ulterior reasons.

The first hero to drop is Ronald Reagan and quite frankly, for me, that was one of the hardest. I was born into a blue stocking Republican household. Pops was a bit of a politico working on various Senatorial campaigns raising money for candidates and working to get out the vote. Reagan was a major hero for him and when I really started looking into the history of how we got to where we are, the core culprit turned out to be the big cowboy himself. You see, what we are dealing with is a direct outgrowth of the S&L crisis of the 80’s which can be put directly at Reagan’s feet. I would like to think it is more of an outgrowth of unintended consequences of well intended acts, but I also have this unfortunate gnawing feeling ….

The next hero to bite the dust was Bush 41. There are lots of reasons to not like the entire Bush family. There is a plethora of circumstantial evidence 41 had his hands in quite a lot of really bad stuff in his long and “distinguished” career but we can set that aside. Bush 41 provided the fixaroo to the S&L mess by taking it “off the books” and setting up the Depository Trust Corporation. This began the set up for what came next.

Eight years of Bill Clinton really did the trick. First we had the Community Reinvestment Act which made it mandatory for financial institutions to lend money into formerly “redlined neighborhoods”. Next, he teamed up with Phil Graham, a particularly nasty republican who has a particularly nasty wife in Wendy (a story for another day), to sign the Graham Bleach Bliley act which retroactively threw holy water on the CitiBank/Traveller’s Insurance merger which was illegal under federal law until their lobbying dollars greased the skids.

Then, in the ultimate set up, he signed, late in his term, the Commodities Futures Trading Modernization Act which legalized the frauds which are now taking place. Then he appointed Wendy Graham, that particularly nasty republican wife of that particularly nasty republican Phil (now working for UBS, one of the particularly nasty villains in this current mess) as head of the Commodities Futures Trading Commission. One of her first acts was to appoint an administrative judge to that commission only after extracting a promise from him that he would NEVER rule in favor of a plaintiff; a promise he fulfilled.”

http://blog.chinkinthearmor.net/?p=900