Re-inflating the bubble

Obama hired back all the Clinton-era officials who caused the housing bust — so they can do it all over again

Donovan now serves as secretary of housing, where media reports say he’s pushing hardest to preserve Fannie and Freddie and its “affordable housing mission.” He believes the mortgage giants facilitate “an important democratization of credit” benefiting “underserved groups.”

ELLEN SEIDMAN: Another architect of the disastrous housing policies that caused the crisis, Seidman actually encouraged subprime lending in “underserved” communities as a top Clinton bank regulator enforcing the Community Reinvestment Act. “Growth in the subprime credit market indicates that credit needs in many low- and moderate-income areas are being met,” she said in 1999.

She also cheered the relaxation of credit standards and the development of the subprime securities market.

“Without CRA as an impetus,” Seidman said, “this market would likely not have developed.”

More recently, she argued it’s “absolutely critical” Fannie and Freddie continue their support for “low-income and minority communities,” despite the mortgage giants’ central role in the crisis. Seidman serves as a director on CFPB’s Consumer Advisory Board, where she’s helping rewrite the rules for home lending. CFPB recently released new mortgage rules that, despite claims of tightening standards, require no minimum credit scores or down payments and even count payments from “government assistance programs” as qualifying income.

Rest here…

~

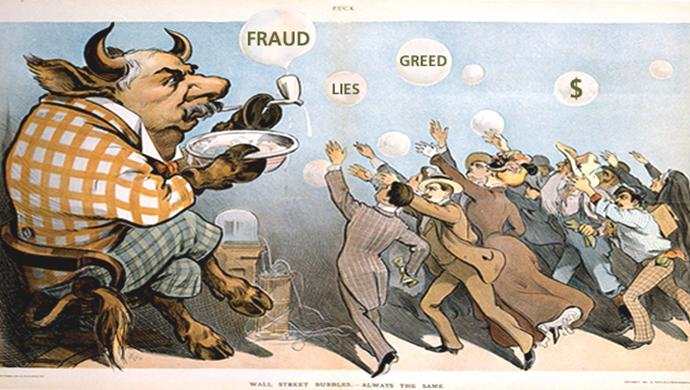

If anyone thinks the industry’s fraud can be easily attributed to those individual’s efforts to provide affordable housing for ‘qualified’ individuals they would be misguided. Banks dumped their risk via credit derivatives. http://www.investopedia.com/terms/c/creditderivative.asp The creation of derivatives For example, a bank concerned that one of its customers may not be able to repay a loan can protect itself against loss by transferring the credit risk to another party while keeping the loan on its books.

If you could sell a house and transfer the loan risk to others and keep the profits, would you do it? A sure thing? Particularly if you could insure the risk and be paid if it fails? Banks find it irresistable even now and want to continue without regulations. Think about underwriting a child who has no responsibility for his actions and the parent (government) must bail him out when he overspends or takes risks. As long as the parent (government) continues to buy out the child’s (bank)mistakes the child fails to learn because he continues to profit from his ventures. The banks were bailed out (don’t forget ‘who’ bailed them out) and warned not to do it again but the profit incentive remains. They took us to the brink before. The methods used, like MERS, to cover their faulty work is being rubberstamped by the Courts every day. Foreclosure laws are being revised to take away homes and re-market them. The bankruptcy courts were never allowed to modify loans. Investors took a hit but if investors gamble on bad products for high yield, they accept risk. They should know better and avoid that risk but as long as insurers deal in underwriting, risk is reduced.

The banks should have failed. Yes, I know chicken little said the country would go over the edge but would it? I wonder if only the banks would have had to restructure and learned a lesson. I don’t think we are out of the woods but the second round of housing failure will be different. The fallout continues to impact the ecnomy. Property taxes are rising. In the end the taxpayers underwrites the wayward children (banks) who fail to take responsibilty for their faulty products that increased yield through risk-penalties that result in a few bucks for those who lost thousands, cost of doing business! These guys made a fortune with their scam! Another sip of the kool-aid? Fannie and Freddie need restructuring, get rid of the fat at the top that uses these entities to feather their own pockets. Both parties missed their chance to pull the industry into line.

Well isn’t this just way too special.