How Housing’s New Players Spiraled Into Banks’ Old Mistakes

Some private equity firms that came in as the cleanup crew for the housing crisis are now repeating ‘errors’ that banks committed, while others are bypassing the working poor.

When the housing crisis sent the American economy to the brink of disaster in 2008, millions of people lost their homes. The banking system had failed homeowners and their families.

New investors soon swept in — mainly private equity firms — promising to do better.

But some of these new investors are repeating the ‘mistakes’ that banks committed throughout the housing crisis, an investigation by The New York Times has found. They are quickly foreclosing on homeowners. They are losing families’ mortgage paperwork, much as the banks did. And many of these practices were enabled by the federal government, which sold tens of thousands of discounted mortgages to private equity investors, (which is the real reason why the foreclosure numbers are down) while making few demands on how they treated struggling homeowners.

The rising importance of private equity in the housing market is one of the most consequential transformations of the post-crisis American financial landscape. A home, after all, is the single largest investment most families will ever make.

Private equity firms, and the mortgage companies they own, face less oversight than the banks. And yet they are the cleanup crew for the worst housing crisis since the Great Depression.

Out of the more than a dozen private equity firms operating in the housing industry, The Times examined three of the largest to assess their impact on homeowners and renters.

Lone Star Funds’ mortgage operation has aggressively pushed thousands of homeowners toward foreclosure, according to housing data, interviews with borrowers and records obtained through a Freedom of Information request. Lone Star ranks among the country’s biggest buyers of delinquent mortgages from the government and banks.

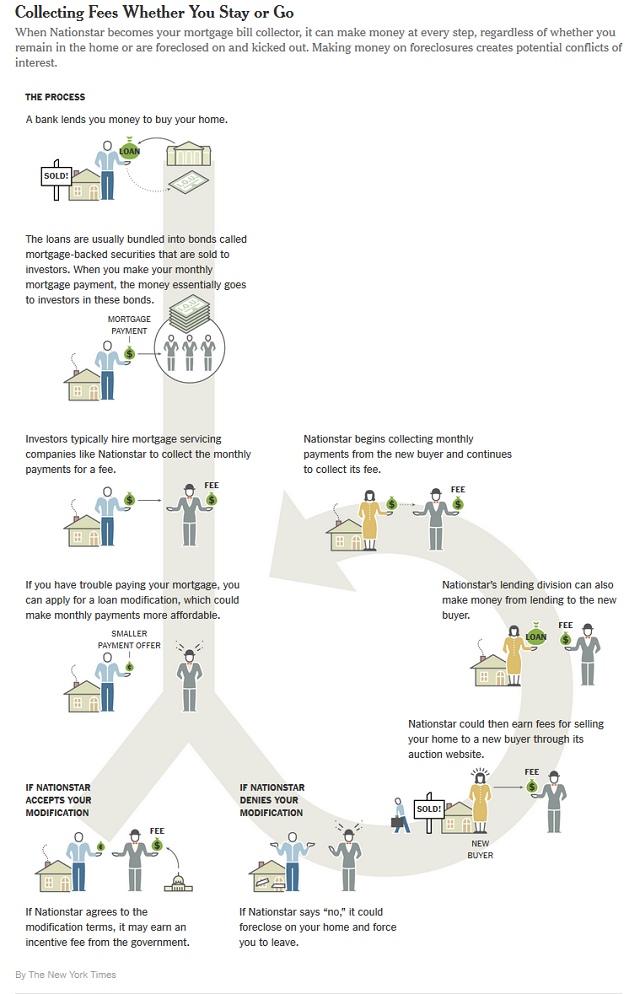

Nationstar Mortgage, which leaped over big banks to become the fourth-largest collector of mortgage bills, repeatedly lost loan files and failed to detect errors in other documents. These mistakes, according to confidential regulatory records from a 2014 examination, put “borrowers at significant risk of servicing and foreclosure abuses.”

Unlike the banks, Nationstar wears many hats at once: mortgage bill collector, auction house for foreclosed homes and lender to new borrowers. By working every angle, and collecting fees at each step, the company faces potential conflicts of interest that enable it to make money on what is otherwise a costly foreclosure process.

Be sure to read the rest from The NY Times here…

A version of this article appears in print on June 27, 2016, on page A1 of the New York edition with the headline: Private Equity Hits Close to Home.

~

Yeah, I know about this since 2009. I trid to apply the TILA “recission” law/rule. AGMSI essentially told me to drop dead and go to hell, for which I did, go to hell from that point forward. After AHMSI refused to respond to all 3 recurn reciept letters (per TILA law I filed pro se suit in my county circut ct. AHMSI did not respond claiming they did not sercive a “summons”. At appro that point I recall the county court granted me a judgement since AHMSI never rreplied to the court or me. AHMSI decided they did not like that so they sent their “henchwoman” hig dollar attorney, Teresa Shill to have an in camera meeting with Judge Horner. She demanded and was granted a hearing in late 12/2009. I have reported this before that when Judge Horner asked Shill “Do you have the NOTE?” she replied “No” with that the judged ismissed AHMSI on basis of TILA “no roop of standing”. House remanded to me “unencumbered” yet in approx 2 years later AHMSI now sold by Wilbur Ross to OCWEN/HSBC filed in Portland Fed Ct and Fed Judge Anna Brown “decided” that OCWEN/HSBC?AHMSI “deserved to take my home and $340k equity. I was “dismiss pro se” from even entering Browns court, with “prejudice. I failed at everything a pro se litigany could possibly do. CFPB seemed to come to my “rescue with 2 billion $ recovery penalty against Ocwen. Its been over 2 years now and the only thing Ocwen has said ie “Opps, we seem to have “lost” your files or missplaced them” Since March this yr they have ignored me while fatas William Ebrey hightails it wit my moneyand many others as well to MALTA. This prick should be immediately arrested, put in custody in chains and brought to justice (if there IS any “justice” as well as chain linking all OCWEN structures complete with all Ocwen employees who aided and abetted fat ass Billie if gutting the uS (and other countries) economies putting thousands of us poor folk so in debt that we can never recover. Nut as Forrest Gumps T shirt says “SHIT HAPPEN” ! What a Christ Almighty shame that federal Judges sided with criminals to protect their interest in ill gotten gains and put you and me out in the gutter, old, disabled with no way out. -30-

Excellent post! Hope many homeowners read! It should be noted Caliber Home Loans is more corrupt than Nationstar. Caliber is owned by Lone Star. Any homeowner subjected the the theft of your home from Caliber should sue for wrongful foreclosure…they don’t hold your debt/dot or note. Examine your paper work and qwr to validate the ‘debt’ immediately. Contact your AG and report their ‘activity’.

The Banks in an act of deception , stole , from the American Homeowner , their personal property ( note) , then proceeded to steal their ” real property ” ( home ) so they could fund their scheme for obscene profits . The correct name for their THEFT is called , THE INTENTIONAL TORT OF CONVERSION . Would you promise to pay an entity back money they never lent you ??? of course not !!! but that is what millions of Americans did , from 2001 to 2006 , when predatory lending was in full swing to fuel the Theft the Banks were performing . after twelve years , I now have the proof of who actually paid off my original mortgage company when I refinanced back in 04 , and it wasn’t the entity that I signed a Mortgage contract with !?!?!? As a matter of fact , it isn’t any of the entities in the alleged securitization documents produced to the Federal Court in my case , which was dismissed with prejudice back in 2013 because , I realized I was being railroaded and refused to cooperate with the direction the Band of pirates wanted me to go . My previous Note holder was paid off by an entity who’s name was never mentioned in the documents associated with my case , with money acquired through what is called ” table funding ” . This Investment Bank , using Investor Money to pay off my original note for the opportunity to use my Note and collateral ( home ) to give value to the certificates sold to these Investors , and without my knowledge and permission , my alleged Mortgage payments every month , went as a cash flow claim to the ” certificate holders ” with the one pretending to be my mortgage company , SERVICING , the flow of money !!!! This is a violation of Federal Law , State Law , and Contract Law , and is subject to rescission under the Truth In Lending Act ( TILA ) which I have performed under operation of Law . This information will be filed with the proper Authorities , and with the Federal Court , asking for a Declaratory Judgement of Rescission Effected !!!!