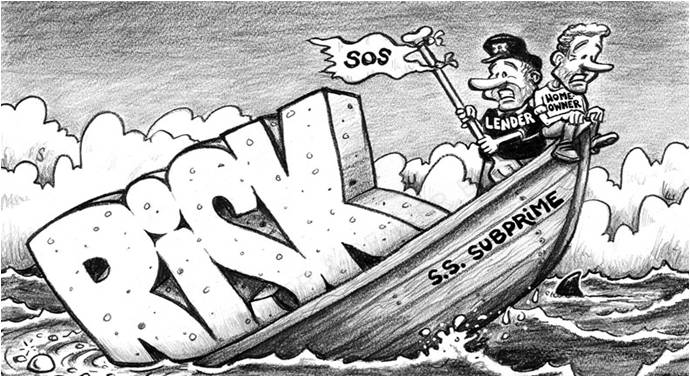

Pundits are Trying to Bring Subprime Mortgages Back. Don’t Let Them

Pundits and think tanks are trying to bring back subprime lending, spinning it as a virtuous move for the economy. Nothing could be more obviously a terrible idea

Mortgages are hard to get, with demands for high credit scores and a perfect lending history, so some say it’s time to bring back subprime mortgage lending.

This is, obviously, a bad idea. The financial industry has plenty of reasons to offer the same high-risk, high-return loans that made so many bankers rich during the housing bubble before everything crashed. But it’s less clear why any sensible commentator wants to cheer the industry on.

Story after story lately follows the same flawed logic: the shoddy lending that caused the financial crisis has now swung too far in the other direction, preventing deserving people from getting mortgages. The poor or middle class can’t access credit, which is the fault of “over-regulation” of banks.

This strange thinking is becoming more prevalent and commanding larger platforms. For example, Binyamin Appelbaum, in a New York Times magazine story this weekend, wondered if subprime mortgages should make a comeback. “The lending freeze is not just preventing people … from chasing their dreams. It’s bad for the overall economy too.”

Maybe this sounds reasonable to pundits. Lending ran too hot, so obviously now it’s running too cold.

But we should question this perceived wisdom. Instead of just buying the false reasoning that self-interested industry lobbyists whisper in an effort to make regulations disappear, maybe it’s time to look at the other factors holding back the mortgage market.

Rest here…

~

If enough people in the same neighborhood borrow 75-100% of their home equity to invest in a small business– and IRS statistics reveal that a great many of those fail within 5 years, right when the balloon payments come due—the 2008 cycle will again repeat, The value of other first time buyers’ homes in that neighborhood will drop drastically within a few months. First time buyers and senior citizens will again lose their equity and find themselves Underwater.

If you are among those who put 20-25% down on a coastal property and went Underwater, even though you weren’t behind on a single mortgage payment, have a high-paying job and excellent credit, you’re wishing you left the funds in your 401-K and rented. And you NEVER want to hear the words “subprime mortgage” again. The same is true of senior citizens who sold a house, then bought a smaller house outright, were up to date on all their bills, and went Underwater because of subprime loans in their neighborhoods. They have no equity left to pay for Assisted Living, and little to no time left to earn more retirement money, even if they’re in good health..

Houses are not ATMS. The British have a saying, “safe as houses.” Let’s make American houses safe again.

If someone needs a loan, they can find investors on the Internet or take out an ad in the local paper. No need to endanger their neighbors’ nesteggs .

Kathleen – first can you point me in the direction of your statement where 75-100% of persons in a neighborhood take out equity to fund small business? I am a mortgage broker and as far as my business model has been in the past most persons who took out equity back before the financial crisis used it for: remodeling, purchase of vehicle, pay down credit card debt, or to settle a divorce situation. Not one of the refi’s that I did in that period had to do with investing in a small business. Those that took advantage of the escalated values for purposes of a reverse mortgage did not suffer any reduction. Second, there is no such thing as an investor on the internet or any type of ad that will produce a loan that does not require collateral such as property. Besides, what is the sole purpose of owning a home in the first place if it’s not to build an equity position for the later years or when you want to sell and move either up or down size? Parents often use equity to pay for their children’s college education or to even help them with a ‘gift’ on a children’s first home. The 2008 cycle, despite what you may think, was not caused by the inflation of values in properties nor the amount of equity loans in a given neighborhood. Your so-called nestegg is built from sales and purchases in and around your neighborhood so in reality it was OTHERS who helped you build that equity. You should be grateful for those that do get mortgages otherwise you would not have any activity in your neighborhood except for cash sales of investors to turn it into a REIT.

Greed is a widely used word these days but it doesn’t always pertain to the bad guys!

For all concerned: I went to the ‘source’ of this article on the Guardian written by David Dayen. Some of the points he makes in the blog are certainly true while others are more or less conjecture an/or suppositions without base or fact. I noticed that there were 14 comments on the blog so I continued to read. The first 13 comments were totally praising the article and when the 14th comment appeared to question the substance of his theory, the comments were ‘closed’ at that point. Strange? If you read the 14th comment by imedina806 the post is asking for clarification and what is said is perfect sense. People, how do we get to the point that once one disagrees the door is shut? Isn’t that the whole point of a democracy? I, too, agree with the points made in the comment by imedina806, so in case it gets deleted at some point soon I am reprinting below:

WAIT a minute guys. If you are talking about Govt Back Mortgages I am with you 100%. But if it is private funds, I dont see the down side on them. For many years “Subprime” loans with common sense underwriting were the stepping stone to many credit affected people into their American dream. There was a 4-9% default ratio in those loans. Loans were made with common sense and nothing like in the 2004-2007 era.

We need to have a very intelligent conversation with these loans as the current PMI’s are killing some people out of the market.