Fair GameA Credit Union That Played With Fire

By GRETCHEN MORGENSON

WHEN Wall Street is accused — as it has been so often these days — of selling risky products to unwitting customers, it usually argues that investors in such exotic stuff are sophisticated adults capable of assessing any hidden dangers.

So it goes with collateralized debt obligations, or C.D.O.’s, which are bonds, loans and other assets that the Street pools together and sells as packages of securities. Purveyors of C.D.O.’s maintain that buyers who lost billions in these mortgage-related instruments were, of course, sophisticated.

But as a recent report from the inspector general of the National Credit Union Administration shows, it is neither credible nor factual that only savvy investors bought C.D.O.’s.

The report analyzes the April 2009 collapse of the Eastern Financial Florida Credit Union. Based in Miramar, Fla., this state-chartered institution was created in 1937 to serve the Miami employees of what later became Eastern Airlines. The institution added other Florida employee groups and was serving 208,000 members when it failed last year.

Eastern Financial had $1.6 billion in assets at the end of 2008. The company was placed in conservatorship on April 24, 2009. It was taken over by the Space Coast Credit Union of Melbourne, Fla. The failure will cost the National Credit Union Share Insurance Fund, the federal agency that guarantees credit union deposits, an estimated $40 million.

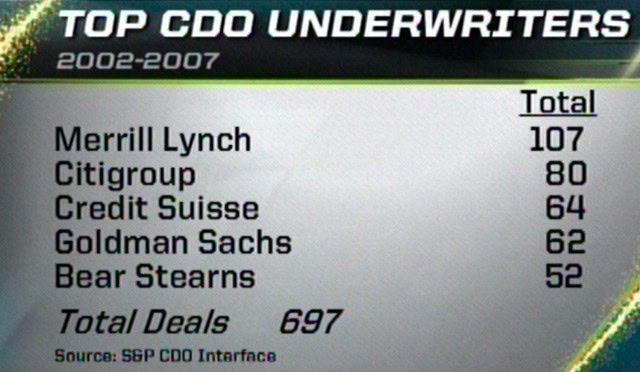

Because it was based in Florida, the doomed credit union had its share of bad real estate loans on its books. But the inspector general’s autopsy report said that the major cause of the Eastern Financial collapse was its decision to dive head-first into toxic C.D.O.’s just as the mortgage mania was faltering.

Between March 2007 and June 22, 2007, the credit union committed nearly $100 million to buy 16 of these instruments; most contained dicey home equity loans.

The timing of these purchases is intriguing. The spring of 2007 was when Wall Street’s mortgage machinery was sputtering; New Century Financial, a big subprime lender, filed for bankruptcy that April. Brokerage firms that had provided funding to lenders like New Century and Countrywide began pulling in their credit lines. At the same time, it became a matter of some urgency for these firms to jettison mortgage-related securities in their pipelines.

Who sold Eastern Financial its toxic securities? Alas, the inspector general identifies neither the C.D.O.’s the credit union bought nor the firms that peddled them.

But the report did note that the instruments Eastern Financial bought were private placements, “which provided less readily available market data to perform analysis and provide better understanding of underlying assets and grading system, tranches, etc.” In other words, the most obscure C.D.O.’s imaginable.

“This situation illustrates yet again why over-the-counter securities and derivatives are not suitable for federally insured banks and other ‘soft’ institutional clients,” said Christopher Whalen, editor of The Institutional Risk Analyst. “Wall Street securities dealers who knowingly cause losses to federally insured depositories should go to jail.”

Credit unions are nonprofit entities and typically do not engage in the risky investing that bank executives did during the credit bubble. Federal credit unions are also limited in the types of securities they can buy. While they can purchase mortgage-backed securities, they are barred from buying C.D.O.’s.

State-chartered credit unions have more leeway to invest in exotic instruments if their home states allow it. Florida, California and Michigan are three such states. But according to the National Credit Union Administration, less than 1 percent of all credit union investments fall into the exotic category.

THOSE state-chartered institutions that can buy C.D.O.’s and other riskier investments must set aside reserves of 100 percent of mark-to-market losses in such securities when they decline in value. This is intended to deter credit union executives from venturing down the risk spectrum.

The Florida credit union met that requirement, but clearly the deterrence didn’t work. Eastern Financial’s failure may be an outlier, but it makes for a terrific case study.

Indeed, the inspector general’s analysis is depressingly familiar. Eastern Financial’s management and board “relied too heavily on rating agencies’ grading of C.D.O. investments,” it concluded, and failed to evaluate and understand their complexity.

Almost immediately after the credit union bought the C.D.O.’s, they fell in value. By September 2007, the credit union had recorded $63.4 million in losses on the products, almost two-thirds of the original investment. By the time of its failure, the credit union had charged off all 18 C.D.O. investments, resulting in total losses of nearly $150 million.

Richard Field, managing director of TYI, which develops transparency, trading and risk management information systems, says the Eastern Financial collapse is yet another example of why investors in complex mortgage securities need to be able to consult complete loan-level data on what is in these pools.

“A sizable percentage of the problems in the credit markets and bank solvency are directly related to this lack of information,” Mr. Field said.

But the Eastern Financial insolvency also illustrates why regulators should make Wall Street adhere to concepts of suitability for institutions as well as individuals, Mr. Whalen said.

“The dealers who sold the C.D.O.’s to this credit union should be sanctioned,” he said. “It might even be possible to pursue the dealer who sold the C.D.O.’s under current law. At a minimum, the Securities and Exchange Commission should impose retail investor suitability standards onto banks and public sector agencies to end the predation by large Wall Street derivatives dealers.”

Will the National Credit Union Administration pursue any of the credit union’s executives or the firms that sold it the toxic securities? “We always consider potential claims of third-party liability in cases of this magnitude,” said John J. McKechnie III, director of public and congressional affairs at the administration.

Remember that with a writeoff, you still own the asset, it just isn’t considered to be an asset any longer. In your example, lets say that someone offers you money for the stock- you can still sell it. This comes into play in the Junk Debt market.

For example, you own Joe’s Bank. Joe’s Bank issues VISA Credit cards. In your portfolio, you have 100 delinquent credit cards with an outstanding debt of $250,000 that have not received a payment in 6 months, so you write them off. You can take that $250,000 loss as a tax deduction, lowering your taxable income by $250K, or you can sell the paper for $2,500 to a Junk Debt Buyer, and still write off the remaining $247,500 against your taxes.

The Junk Debt Buyer ( a type of collection agency that buys debts that are in default, rather than collecting them under contract) then attempts to collect on the full face value of the $250,000. Often, they will go after anyone they can using any tactic they can, even people who do not owe money, but whose names are similar to the true debtor. These tactics are not legal, but the chances of getting caught are almost zero, because most consumers don’t know their rights, and the shame of being chased by a debt collector often prevents them from seeking help. The FTC is charged with enforcing the laws on this, but they rarely do anything.

What this means for the Junk Debt Buyer is that if they collect on even a few of the 100 credit cards, they are in profit territory. The Junk Debt Market is one of the fastest growing segments of the financial industry. Many of these portfolios allow profit of up to 5,000%.

Sub-prime debt, and the illegal tactics used in enforcing it, are very lucrative.

Upon reading the above, I emailed a friend. “I am still working on understanding CDOs vs MBS, but if “By the time of its failure, the credit union had charged off all 18 C.D.O. investments, resulting in total losses of nearly $150 million.” does that mean that the mortgage debt is “charged off”? How does this tie into the outstanding principal balance due on a note backed by a mortgage?”

She emailed back:

“Your Basic WriteOff:

Lisa boys stock in AT&T. Stock is worth $100,000.

Lisa fills out a Financial Statement listing her assets and her debts. She lists as an asset $100,000 in AT& T Stock.

AT&T phones prove to be cancer-causing – bottom drops out of the market. Lisa’s stock is now worth $ 00.00

Lisa fills out a financial statement – she must “write-off” the value of the stick – that is, she can no longer claim it as an asset because now it is worthless. (But if she also had stock that soared in value, she can use her losses to pay less taxes on her gains.)

__________

CDO:

Lisa’s Swell Securities (LSS) buys shares in 10 different Residential Mortgage Backed Securities Trusts. LSS buys the lowest, riskiest level (called tranches) LSS then makes an investment vehicles out of its purchases. The assets in this LSS are the shares of the 10 different RMBS. So the CDO doesn’t own any properties itself – it owns shares of the trusts that own the properties.

__________

SWAPS

LSS realizes it owns some pretty iffy shares. LSS goes to AIG and says: sell us a policy that if our grand plan to make money investing in the riskiest level of these 10 trusts does not work out – and we actually lose money, when we are down 40%, the insurance company will be required to reimburse us for any further losses.

Now the insurance company has taken on the bad risk created by LSS. Or has “swapped” with LSS – taking much of the risk in exchange for a nice hefty insurance premium.

__________

WHAT IF THE riskiest properties were even riskier than disclosed? What if each of these properties was purchased by some crooks who were telling big fat lies about the qualifications of the buyers? AND what if the trust never obtained any notes or assignments so they absolutely could not successfully foreclose. The investors in those lowest levels would see their investment fall to zero value.

And if you were pitiful enough to have bought the CDOs put together by LSS (a collection of the riskiest levels of 10 different trusts) then you also have ZERO value – AH, but wait, where is that insurance policy – AH, right here – OK, AIG, we will take our losses up to 40% – but the next layer of losses – the 60% – you must reimburse us for all of that because we “swapped” risk for premium.”