Click to Enlarge

The 2012 Long-Term Budget Outlook

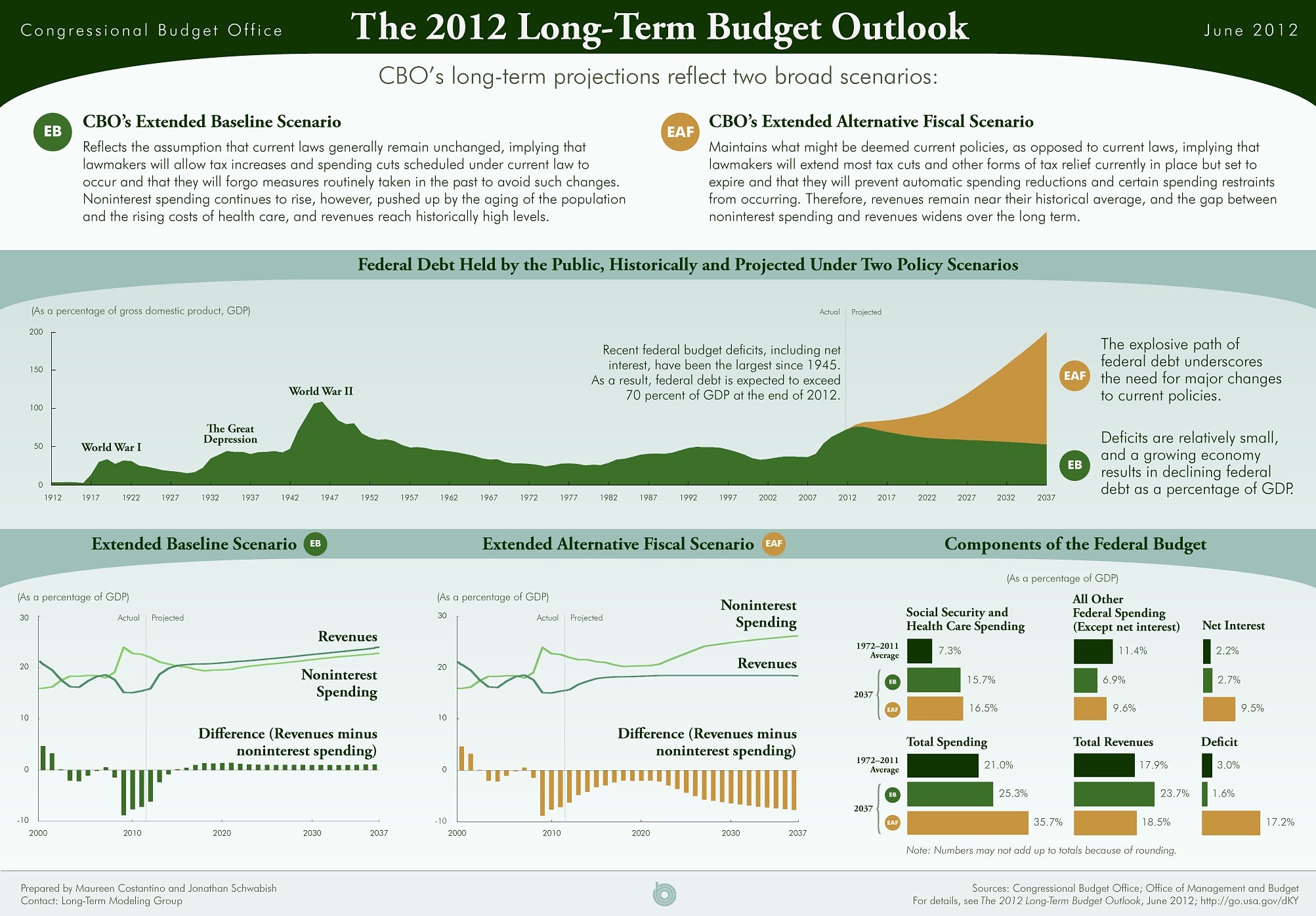

Over the past few years, the federal government has been recording budget deficits that are the largest as a share of the economy since 1945. Consequently, the amount of federal debt held by the public has surged. By the end of this year, CBO projects that the federal debt will reach roughly 70 percent of gross domestic product (GDP), the highest percentage since shortly after World War II.

Whether that debt will continue to grow in coming decades will be affected by long-term demographic trends (particularly the aging of the population), economic developments, and policymakers’ decisions about taxes and spending.

What Are Some Key Elements Underlying the Fiscal Challenges Facing the United States?

The aging of the baby-boom generation portends a significant and sustained increase in the share of the population receiving benefits from Social Security, Medicare, and as well as long-term care services financed by Medicaid. Moreover, per capita spending for health care is likely to continue rising faster than spending per person on other goods and services (although the magnitude of that gap is uncertain). Providing the health care services and retirement and disability benefits that people are accustomed to will consume a greater share of the economy in the future than it did in the past.

Specifically, if current laws remained in place, spending on the major federal health care programs alone would grow from more than 5 percent of GDP today to almost 10 percent in 2037 and would continue to increase thereafter. Spending on Social Security is projected to rise but much less sharply. Altogether, the aging of the population and the rising cost of health care would cause spending on the major health care programs and Social Security to grow from more than 10 percent of GDP today to almost 16 percent of GDP 25 years from now. That combined increase is equivalent to about $850 billion today. (By comparison, spending on all of the federal government’s programs and activities, excluding net outlays for interest, has averaged about 18.5 percent of GDP over the past 40 years.)

What Policy Scenarios Did CBO Analyze?

In this report, CBO presents the long-term budget outlook under two scenarios that embody different assumptions about future policies governing federal revenues and spending and present very different pictures of future budgetary outcomes.

Below is a table summarizing those scenarios.

The two scenarios span a wide range of possible policy choices, and neither represents a prediction by CBO of what policies will be in effect during the next several decades.

What Is the Budget Outlook Under the Extended Baseline Scenario?

Under the extended baseline scenario, which generally adheres closely to current law, federal debt would gradually decline over the next 25 years—from an estimated 73 percent of GDP this year to 61 percent by 2022 and 53 percent by 2037. That outcome would be the result of two key sets of policy assumptions:

- Under current law, revenues would rise steadily relative to GDP because of the scheduled expiration of cuts in individual income taxes enacted since 2001 and most recently extended in 2010, the growing reach of the alternative minimum tax (AMT), the tax provisions of the Affordable Care Act, the way in which the tax system interacts with economic growth, demographic trends, and other factors; revenues would reach 24 percent of GDP by 2037—much higher than has typically been seen in recent decades—and would grow to larger percentages thereafter.

- At the same time, under this scenario, government spending on everything other than the major health care programs, Social Security, and interest—activities such as national defense and a wide variety of domestic programs—would decline to the lowest percentage of GDP since before World War II.

That significant increase in revenues and decrease in the relative magnitude of other spending would more than offset the rise in spending on health care programs and Social Security.

What is the Outlook Under the Extended Alternative Fiscal Scenario?

The budget outlook is much bleaker under the extended alternative fiscal scenario, which maintains what some analysts might consider “current policies,” as opposed to current laws. Federal debt would grow rapidly from its already high level, exceeding 90 percent of GDP in 2022. After that, the growing imbalance between revenues and spending, combined with spiraling interest payments, would swiftly push debt to higher and higher levels. Debt as a share of GDP would exceed its historical peak of 109 percent by 2026, and it would approach 200 percent in 2037.

The changes under this scenario would result in much lower revenues than would occur under the extended baseline scenario because almost all expiring tax provisions are assumed to be extended through 2022 (with the exception of the current reduction in the payroll tax rate for Social Security). After 2022, revenues under this scenario are assumed to remain at their 2022 level of 18.5 percent of GDP, just above the average of the past 40 years.

Outlays would be much higher than under the other scenario. This scenario incorporates assumptions that through 2022, lawmakers will act to prevent Medicare’s payment rates for physicians from declining; that after 2022, lawmakers will not allow various restraints on the growth of Medicare costs and health insurance subsidies to exert their full effect; and that the automatic reductions in spending required by the Budget Control Act of 2011 will not occur (although the original caps on discretionary appropriations in that law are assumed to remain in place). Finally, under this scenario, federal spending as a percentage of GDP for activities other than Social Security, the major health care programs, and interest payments is assumed to return to its average level during the past two decades, rather than fall significantly below that level, as it does under the extended baseline scenario.

What Is the Impact of Growing Deficits and Debt?

The projections discussed above understate the severity of the long-term budget problem under the extended alternative fiscal scenario because they do not incorporate the negative effects that additional federal debt would have on the economy. In particular, large budget deficits and growing debt would reduce national saving, leading to higher interest rates, more borrowing from abroad, and less domestic investment—which in turn would lower the growth of incomes in the United States.

Taking those effects into account, CBO estimates that gross national product (GNP) would be lower under the extended alternative fiscal scenario than it would be if debt remained at the 61 percent of GDP it would reach in 2022 under the extended baseline scenario. The reduction in GNP would lie in a broad range around 4 percent in 2027 and in a broad range around 13 percent in 2037. (Under the extended baseline scenario, GNP would be nearly identical to what it would be if the nation’s debt burden remained constant.)

Rising debt also would have other negative consequences beyond those estimated effects on output. It would:

- Result in higher interest payments on that debt, which would eventually require higher taxes, a reduction in government benefits and services, or some combination of the two.

- Restrict policymakers’ ability to use tax and spending policies to respond to unexpected challenges, such as economic downturns or financial crises.

- Increase the probability of a sudden fiscal crisis, during which the government would lose its ability to borrow at affordable rates.

What Can Policymakers Do?

The explosive path of federal debt under the alternative fiscal scenario underscores the need for large and timely policy changes to put the federal government on a sustainable fiscal course. Policymakers will need to increase revenues substantially above historical levels as a percentage of GDP, decrease spending significantly from projected levels, or adopt some combination of those two approaches. In fact, the current laws that underlie CBO’s baseline projections provide for significant changes of those kinds in coming years; many other approaches to constraining future deficits are possible as well.

But policymakers face difficult trade-offs in deciding how quickly to implement policies to reduce budget deficits. On the one hand, cutting spending or increasing taxes slowly would lead to a greater accumulation of government debt and might raise doubts about whether longer-term deficit reduction would ultimately take effect. On the other hand, abruptly implementing spending cuts or tax increases would give families, businesses, and state and local governments little time to plan and adjust, and would require more sacrifices sooner from current older workers and retirees for the benefit of younger workers and future generations. In addition, immediate spending cuts or tax increases would represent an added drag on the weak economic expansion.

Full report below…

~

4closureFraud.org

~

The 2012 Long-Term Budget Outlook

Well, after the Lan Pham incident – do these fine folks retain 100% credibility?