No Appeal—The Success of HAMP and the Independent Foreclosure Review

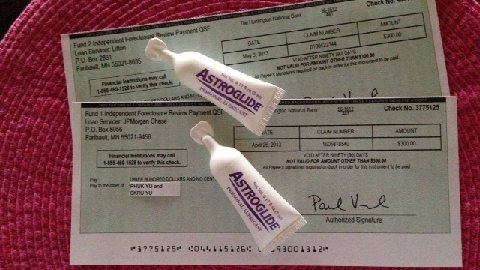

Well, now, that’s over. $300. And…the check bounced. Ah, but what the hell; easy come, easy go, eh?

Four years after the discovery that:

bankstas created and channel stuffed exotic mortgage loans designed by their Wall Street Risk Analysts to guarantee their failure,

coupled those designed to fail loans with vastly inflated appraisals,

referenced these inflated, guaranteed to fail loans which they themselves described as “shit” repeatedly in numerous mortgage backed securities,

sold slices to pension funds as triple A when they were, in fact, designed specifically to fail,

bet against the mortgages performing because they knew they could make them fail,

got rich destroying the global economy,

numerous investigations have been completed all concluding that the foreclosure crisis was manufactured by Wall Street,

numerous law suits have been settled for pennies on the dollar without any admission of wrongdoing,

consultants, lawyers and various governments have received billions,

bought most of the media so they could blame all of the world’s problems on the victims, and then write them a check for three hundred dollars….that bounces.

Everything worked out perfectly, for bankstas. All neatly wrapped and shoved aside, the brutal financial rape of the middle class has neither been punished nor discouraged, and continues unabated.

To the victims, people like Michelle Norris of Temecula, CA, who was the victim of an escrow account scam at Wells Fargo, that $300 is a slap in the face, the final insult, and absolute proof that bankstas and their elected minions have destroyed America’s legal system beyond repair. For the citizens of this country, it means that revolution and not redress is inevitable.

She was cheated and turned to every government regulator for help. She had an enormous three ring binder with all of the documentation showing Wells Fargo’s outrageous conduct and no one would act to help her. Michelle, like most victims of fraudclosure in California, couldn’t find a lawyer who wanted the case. Reminds me, I wonder whatever happened to Catherine Porter, the California Monitor? Why does it even matter?

What about Heidi McCarthy, formerly of Delaware, whose home was destroyed by flooding and turned out to be in an undisclosed flood plain, which resulted in a cover-up, foreclosure and threats from government agencies as she tried to pursue her claims?

What everyone skips over is that a large number of foreclosures were created by the servicers, see https://www.realtown.com/gwmantor/blog/predatory-loan-sevicing-part-one, https://www.realtown.com/gwmantor/blog/predatory-loan-serving-fraud, https://www.realtown.com/gwmantor/blog/fraud-servicing-opportunity

I know hundreds of people like Michelle and Heidi. The Bank’s narrative that people are deadbeats couldn’t be more wrong. I work the other side of the street trying to help people stay in their homes, and you can take my word for it, most people would do anything not to lose their home, but the banks wanted no other outcome than a default.

HAMP and The Independent Foreclosure Review are among the best examples of a government consciously, willfully, and maliciously selling out its people and destroying the very fabric of America. This is real terrorism, not virtual terrorism.

These were programs allegedly intended to help the American people who were either direct or indirect victims of banksta fraud. Fraud, not paperwork errors but active, planned fraud! Get it and don’t forget it.

Numerous studies have now confirmed what many of us suspected, the Home Affordable Mortgage Program (HAMP) was such a miserable failure that it could only have been intentional and that the Independent Foreclosure Review was a failed attempt to cover up a massive criminal enterprise.

Pay very careful attention to what I am about to tell you: HAMP was conceived to accelerate foreclosures not prevent them, and the Independent Foreclosure Review was not independent but was conceived to bury evidence of systemic, criminal activity.

We now know for absolute certain that millions of illegal foreclosures involved borrowers who were not in default and were based on forged paperwork.

Yes, they did, Business Pro; yes, they did.

Several county recorders have audited their foreclosure files and consistently found false documents evidencing premeditated, criminal fraud in 84% of foreclosures, not the 6.5% originally announced by those lying motherfuckers at the OCC.

Phil Ting, the San Francisco assessor-recorder, examined files of properties subject to foreclosure sales from January 2009 to November 2011. According to Ting, 84 percent of the files contained what appear to be clear violations of law, and fully two-thirds had at least four violations or irregularities.

Do you believe that San Francisco is any different than any other county? It’s all routine, everywhere, mostly done by machines and foreign workers following a manual.

After the deadline for homeowners to submit their paperwork for the Independent Foreclosure Review, the OCC and the SEC realized that the banks were concealing the evidence being found by the reviewers and simply pulled the rug out from under people who had already had a similar experience trying to get a HAMP modification. Send a mountain of paperwork and the servicers just send it off to India where it fuels tandoori ovens.

Lorraine Brown of Lender Processing Services admitted to forging more than one million false documents used in illegal foreclosures. The victims get $300.

We are told that it cost $20,000 a file to review the documents. Bullshit! I can do it in five minutes. Everyone thinks it’s so complicated but you only need a handful of documents to see exactly what is going on. For an anatomy of a fraudulent foreclosure go here: https://4closurefraud.org/2011/06/28/george-mantor-robo-signers-a-tangled-web-indeed/

A question to regulators: when you abet such high level criminal activity, don’t you ever fear for the lives of your children? You are destroying their future…or do you even fucking care?

That forged paperwork is currently the focus of a battle between congress, mostly Elizabeth Warren, and the SEC which argues that those forged documents are…get ready for this…”Trade Secrets” of the banking industry.

Trade secrets? No they aren’t. They are reports of public transactions, they speak for themselves and most of them are recorded. Come on, now. Stop lying and covering up criminal activity.

Regulators and government officials who are involved in these activities are all traitors and should be shot on-site. Does anyone disagree?

Remember, we are talking about a massive global Ponzi scheme in which residential and commercial real estate, car loans, credit cards, student loans, commercial leases, and related debt were pushed all over the planet so that central banks could create more debt based money. The commercial real estate defaults haven’t even started yet, but they will be coming next because failure is the new success.

You have to understand the bigger picture and the connection to fractional reserve banking and fiat money or everything seems counter intuitive. When you know that the money is actually worthless and is simply being bet in large quantities like casino chips frauds is inevitable.

I used to wonder, why are banks working so hard to avoid foreclosure workouts? There really are better alternatives for a borrower in distress than foreclosure. It was the defaults they wanted, not a workout. Enter HAMP.

When the government announces a new program to help Americans, I always ask, “what is the real problem they are trying to solve, and who is really behind this?”

Most Americans don’t lobby for new government programs to help them…we’ve already learned our lesson. But, the corporatocrocy knows what it wants and how to get it– government programs.

More and more, when you peel back the layers of the onion what you often find is a program that was conceived and influenced by special interests in private enterprise.

Back in early 2009, when President Obama introduced his signature relief plan to stem foreclosures, the Home Affordable Mortgage Program or HAMP, I’ll admit that I was skeptical.

And indeed, quarterly report after quarterly report shows that foreclosures, which HAMP was purportedly created to reduce, have gone up dramatically with very few actual modifications ever done.

Chris Wyatt from Litton Loan Services describes an atmosphere in which employees were instructed to avoid modifying loans and instead to dual track the applicants into foreclosure.

Remember, when we think about the elements of this global Ponzi scheme of bonds backed by fiction, nothing is obvious and logical. They don’t call it shadow banking for nothing. But, it’s more like a parallel universe where everything is the opposite of what seems logical.

Bankstas don’t get rich for having brilliant ideas or making something of value, they get rich for doing something far simpler. They get their money for fomenting failure. For them to win, people must fail, companies must fail, villages must fail, cities must fail, and counties must fail. Greece, Cyprus, Spain, Portugal, Italy, Ireland, and the United States must all fail. If they win, we all must lose. The very purpose of Central Banking has always been to economically enslave us.

Through that prism, the very purpose of HAMP becomes crystal clear. There are only a few requirements to obtain a HAMP, presumably to help more people. But, one of the requirements was that the borrower had to be in default on their payments.

Why? Why does that matter? The only criteria weighed for approval was the borrower’s income so why couldn’t a borrower get a modification without missing payments?

Qualifying for a HAMP is all numbers driven. If you hit the numbers, you qualify for HAMP. You have to reveal your financial situation anyway from which it can be easily deduced that the payment is too high for the monthly income and should be reduced accordingly. That’s HAMP. No principal reduction and a longer loan.

But, the banks had no real interest in stemming foreclosures; just the opposite.

The real problem for banks wasn’t that there were too many foreclosures; the problem was that there were not enough and there still aren’t. That is why they keep on pushing borrowers into default, they don’t even have to foreclose, they just need enough defaults to declare the pool in default. And, that is why, despite all of the settlements, the bankstas go right on doing the same things every day. Nothing has changed and why would it?

Except for the great depression, a few pockets of economic decline, and timeshares, foreclosures have been exceedingly rare in the United States. For decades, the foreclosure rate hovered around three tenths of one percent.

The mortgage pools had a default threshold of 8%, which made them seem bullet-proof to default. Eight percent of the mortgages would have to fail before the pool would be considered in default. At that point, the pool stops forwarding payments to the investors and credit default swaps pay multiple times the amount of the loans in the pool.

That was the way it was supposed to work. Buy a fire insurance policy on every house in the neighborhood (Credit Default Swap) then burn down the neighborhood (create defaults).

But, and it’s a big but, despite the fact that Wall Street actuaries designed new types of loans with features that statistically should have increased defaults, even though many of the loans had no real borrower and no payments on the loans were ever made, it wasn’t enough to hit the threshold. Even by massive value appreciation and steep decline, it wasn’t enough. Even with the crashing recession that cost many borrowers their livelihoods, it wasn’t enough.

Americans stubbornly continued to scrape together the cash to make their payments even after property values collapsed. That is the real story here and it never gets told.

That was the problem that HAMP was created to solve. There were not enough mortgage defaults to default the entire pool of loans. The loans were created to fail, designed with exotic new terms by people who study risk for a living. And yet, the American homeowner was hanging on. They hung on through forced place insurance, through onerous forbearance agreements, through property tax schemes. Sure people were losing their jobs, and yet they hung on by their fingernails.

HAMP was conceived to lure in the thousands of people who, come hell or high water, made their mortgage payment and had no intention of defaulting. But, now they had them on what we now know they called the “dual track.”

Servicers mass mailed borrowers and in came the calls. Was it really true? Was there really a way to lower my payments? The answer is no, not with HAMP. The program was designed with a poison pill. No HAMP if you are current on your mortgage.

Why? What about those people who did the right thing and sacrificed and found a way, but desperately need relief?

They were told to stop making their mortgage payment and call back in three months. Gotcha! One of the most common types of foreclosure is the “Dual Track”. The borrower is encouraged to stop making his payment to meet the default qualification to obtain a HAMP.

As soon as the third payment is late, the servicer files a notice of default to start the clock running and moves directly forward before the borrower even begins the modification process.

In the case of large Goldman Sachs Servicer, Litton, they never intended to do any modifications. They simply shipped all of the modification paperwork to India.

Litton programmed its voicemail system so that it would disconnect borrowers who were in default and trying to get their loan modified before the trustee’s sale. The system asks for the loan number and the last four digits of the borrower’s social security number. Once these are inputted, the system responds that there is no record of that loan and hangs up. Clever, eh?

As to the independent foreclosure review, this, my friends, is the piece de resistance in the entire global Ponzi scheme. More aptly it should have been named “The Sell Out and White Wash”. Collect mountains of paperwork from the victims showing a consistent pattern of massive fraud and collusion; give them each a check for $300 and burn the evidence inside the regulatory agencies. Stamped on the check in bold letters, “NO APPEAL”.

Agency employees move on to lucrative jobs with the entities they regulated and people who had as much as hundreds of thousands of dollars in equity stolen get a check for $300.

Are we really supposed to accept that? Really? That’s it? This will make the history books and the real story will be known to everyone. The bankstas may have won but their names will be referred to in the context of serious evil.

When the legal system is completely broken, filing claims and going to court gets you absolutely nowhere but chewed up and spit out. No more polite talking with judges, the fix is in.

It’s time to start killing bankstas just as a matter of self-preservation. Vigilante justice is the only justice left to us. If our government employees refuse to regulate these institutions and our tax paid prosecutors are afraid to prosecute them, then it’s time for us to start taking matters into our own hands and even the score.

Come on now all you camo-coated ammo stackers, you night-scope toters, you multi-mag marauders, you big-bore blowhards and those of you living in bunkers, go blast a banksta and make the world a better place. Isn’t this the moment you’ve all been waiting for?

If you are angry and disenfranchised, don’t go shooting up schools and cinemas and blowing up public gatherings, take it to Wall Street, Capitol Hill, and their country clubs and yacht marinas.

We have seen the enemy and he believes that he is invincible.

Central banking, fiat money, and global grand theft have nearly cost us our freedom. We pay taxes to a government controlled by central banks and the results suggest only one of two possibilities: massive corruption or dangerous incompetence.

Two recent reports found that Americans are more afraid of their government than terrorists and rightly so, there are no other terrorists. By virtually any measure, the results produced by government are an across the board failure with the respect to their constituents. If you understand the above, then you understand that the entire war on terror was conceived to terrify us. The war is on, will we ever fight back?

Remember the words of Thomas Jefferson, “The tree of liberty must be refreshed from time to time with the blood of patriots and tyrants.

~

I echo the statement that this article is the best written on the subject. It ought to be required reading in US history books.

I’ve had a lot of practice on mortgage mod-packages. I can now quickly round-up the requisite current financial data & have refined my hardship letter so all the pertinent details are in as brief a write-up as possible.

My servicer is Ocwen & Freddie owns my loan. I’m 2 to 3 mos behind & re-setting the foreclosure review letter month to month with my payment now.

Bought new house in ’07 & planned to re-fi once old house sold…we got STUCK with our old house 4 years…lost $40k trying to carry both mortgages & eventually rec’ a chap7 discharge in 2010. Final irony is the old house sold the following summer (short-sale). Now stuck @ hi rate & payment.

I can’t qualify for HARP because I’m late. Can not & WILL NOT re-affirm the debt, so Freddie says no-way on a principal forbearance (they do not do princ-reductions) and was denied HAMP because our debt to income was too-low (26%…just under the required 31%). Now that they CHANGED that ratio requirement I WAS gonna petition to be re-considered for HAMP. This article tells me there is nothing I can pursue I guess?

Who might actually take 3 mins to review my details over a cup of coffee & point me in the direction of how to proceed? I don’t have a lot of $, but would be willing to pony-up for good, useable advice. I have tried using the gov’t approved counselors & so-far they’ve all been absolute flakes…

While I agree with much of what your article says and can honestly say I am truly disappointed in the the results of the Independent Foreslosure (IFR), it’s time to set the record straight on the “consultants”. The quotes in the media makes my blood boil every time I read another article that “billions” was spent on the (IFR) and the “consultants” lined their pockets. “For the record; I truly hope this is quoted because I was a Consultant.”

“Consultants did not get billions or line their pockets.”

“Consultants did not bill for their services.”

“Consultants were paid a flat rate hourly wage; a stipend for meals and actual expenses while away from home working on the IFR project.

“Consultants worked at a flat hourly rate; without the benefit of overtime pay even when working over 40 hours a week – and there were many over 40 hour weeks.”

“Consultants didn’t get paid holiday time and we worked many holidays. If a Consultant didn’t work, there was no pay.

“Consultants went home and got to stay 4 days with family at home out of every month while working on the IFR project.”

“Consultants spent months away from home and counltess hours wading through documents and reporting the findings, pro or con to management and the applicable agency.”

“Consultants did not make policy, change policy, change procedures, talk to, cater to or have direct contact the servicing company or banking institution during the IFR process.”

“Consultants were subject matter experts with decades of experience in the industry.”

“Consultants are prevented from speaking out, disclosure, or discussion about the IFR and are bound by confidentiality agreements that prevent us from talking.”

“Consultants truly believed in the task assigned and the responsibility that dealt with the IFR process.”

While I could continue, the point has been made that Consultants did not make billions, spend billions or line their pockets. Consultants did the tasks they were given. Much has been said about the process not being truly independent. Speaking for myself and those I worked with, every review was done without influence, was strictly based on the facts and was reported accordingly. The IFR process was extensive, time consuming and yes expensive. The Consultants worked for “companies” that billed for the IFR. The Consultants do not know what the companies we worked for billed, for our services.

Consultants have taken a real beat down over the IFR. Walk a mile in my shoes! Do what I did for months! Be a subject matter expert, for the pay I received! Add to that; the task and responsibility for review of more than 4.3 million consumer mortgages/complaints. Get beat up daily with reports by the news media about what a lousy job Consultants did! Be part of a process that had never been done in the history of mortgage lending, and then tell me….. Where is the billions of dollars, I as a Consultant received? I really would love to retire, travel the world and live a billionaire’s life with all that money I can’t see in my bank account.

Hi, I understand your task and would’nt want to walk a mile in your shoes. However, I do know that the Executive Jack Lew of Citi was paid a great bonus before leaving Citi after the bailout, and was able “travel the world and live a billionaires life” then invest heavily in the Rust Consulting. I am sure the pay was little for you workers and the task was long and hard, after all thats what Corporate greed is all about. I do believe that my file and countless others of Citi were not properly reviewed, how else do you explain a Bank of America client was in the same exact situation as myself in the same year, she was reviewed, received a settlement payout, still in her home. I, a CitiMortgage customer did not get reviewed and was told I had to been foreclosed on before it could be review.(Wrong) The only line I can draw is maybe Citi did not have as many of their files reviewed, because after all these banks ended up policing themselves. Which brings me to the question can we get the exact details of the IFR from each bank? Nevertheless to me Mr.Lew our US Treasurer Secretary had a conflict in interest and should not have been appointed to his position after investing heavily in Rust Consulting.

Your articles have been great! I have written everyone I can think of concerning my issue with the IFR. I would love to know how many Citi customers were a part of the IFR. Citi was my bank and I was told even though I was sent letters of intent to foreclose this settlement did not include me. Even though the criteria was listed on the website and I fully fit criteria, Citi says its a little confusing to customers and you had to have a foreclosure completed on property during 2009. Wrong! A co-worker is a BOA customer, was sent letters such as myself and was included in the review. Am I reading to much into this or is it a coincidence that Jack Lew (US Treasury Secretary)who received a very large bonus after the big bank bailout, was a stake holder in Citi, then months later become a major investor in Rust Consulting, do it benefit this company to deny reviews who are intitled to a review? How many CitiMortgage clients were processed? This just dont seem right that a major investor is in US Finance Chair.

G.W.,

Thank you for your relentless fight against the evil and corrupt systems in place.It is quite apparent that those in power will stop at nothing to unravel and burn the fabric of our society.

My question is this:how do we proceed from here?

So many are asleep,numb and complacent about the war being waged against everything we hold dear!We are dealing with invisible,conscienceless entities whose primary goal is to swallow up the masses and leave nothing alive in their wake.

I cannot even get my friends (save but two) to even take enough interest in this situation to read your magnificently brutal article!The truth hurts;so everyone turns a blind eye-brainwashed into believing they will be safe if they ignore the truth.

Ignorance is bliss;but it is no excuse to destroy the hope of future generations.We are not fighting against this for today;we are doing so because we realize the ripple effect that will occur if we do nothing to fight against it.

“When unwritten laws become written laws,the liberty of man begins to suffer”.

~Thomas Jefferson

Guess some of us have not yet suffered enough to stand up against this tyranny.

~Heidi M. McCarthy

It WILL NOT end until we demand it to end. #1 who voted for O. sorry but, any sitting president that is directly responsible for me in litigation / foreclosure because of bank fraud. does not deserve my vote. I just dont get it. WE WERE TOLD BY O TO ASK OUR BANK FOR A HAMP LOAN. none of us new what a servicer was or that our mortgages were sold. that is mortgage fraud. then told not to pay the mortgage that is breach of contract. then they robo sign, and robo stamp documents, fraud. kets not forget the above article approving mortgages designed to fail with wrongful appraisals.

I received the below email today

Some have inquired what do you say when they have not produced the actual note yet but only uncertified copies of it?

Some of that would depend on whether there were endorsements on the note copy and whether they were specific or blank endorsements.

If specific and the party who is the endorsee is not the one claiming rights to enforce it is a fairly simple argument to make that their own exhibits bely their standing to claim rights to it since it is endorsed to another legal entity. If it is a blank endorsement the question becomes how old is this copy. If it was endorsed in blank by the original lender way back when the loan was made, anyone could have it now and such a copy is evidence of nothing without a certified copy showing when it was made.

If it is known the loan has been transferred but there is no endorsement then it is obvious this is an old copy made prior to the first transfer and again is evidence of nothing. And you can testify ahead what you do know to be true concerning the original note you signed:

Affiant has no knowledge of facts to the contrary, the original note contains Affiant’s fingerprints as may be determined by any document analysis expert of Defendant or of the plaintiff which have yet to examine the document and make authoritative testimony accordingly.

Afflants also state upon best belief and knowledge new computer technologies can and have been used to detect any photo processing that might exist in the making of these documents if need be to ascertain authenticity.

Affiants declare first hand eye witness knowledge of the fact that the original note signed November 21, 2006 was signed in blue ink by the Plaintiffs.

Affiants affirm that on the original promissory note will be found the pressure imprint of their signatures which affiants here affirm they specifically recall being present on the actual note signed that day of the closing.

And there may be more you can say than this. If someone has a similar situation we can talk about what may be in your case. You may reach us at 214-230-0319. Dr Weatherly

Nice summary. No need for violence, that’s what Bankstas want. The best thing for rage is to calmly survey the matter, turn our backs and walk away, then they disappear.

Alternatives like Public Banking, a la Ellen Brown, cut out the Bankstas.

Outstanding journalism, finally, on how the shell game works. Effective response – Chapter XIII! Next is armed conflict…

George, you always outdo even yourself. However, if you want people to revolt, I wish you would suggest a peaceful, rather than a bloody, revolution!

Great article. I think we haven’t heard the end of the HAMP failure story either – When the massive balloon payment is due at the end of 25+ years, and even if the payment is made, a clouded title remains.

PS: Don’t forget Bush Jr. had the first program – called HOPE for Homeowners in 2008.

– Still hanging by fingernails here.

This is the best article on the mortgage fraud debacle I have ever read. The summation in your words—-“Everything worked out perfectly, for bankstas. All neatly wrapped and shoved aside, the brutal financial rape of the middle class has neither been punished nor discouraged, and continues unabated.” Oh, if only we could hold those responsible and make them pay.

A viral spoof tells one man’s TRUTH. “Die Banker Die”: http://www.youtube.com/watch?v=YGFZ1Jj3ui8