“Put simply, it’s time to lend again to borrowers with less-than-perfect credit.”

~

Squeaky-Clean Loans Lead to Near-Zero Borrower Defaults-And That is NOT a Good Thing

There’s something interesting and important going on in the mortgage market today: borrowers who took out mortgages in the past five years have rarely defaulted, making them better at paying their mortgages than any other group of mortgage borrowers in history.

This is happening for two main reasons: only the best borrowers are getting loans today and these loans are so thoroughly scrubbed and cleaned before they’re made that hardly any of them end up going into default. A near-zero-default environment is clear evidence that we need to open up the credit box and lend to borrowers with less-than-perfect credit.

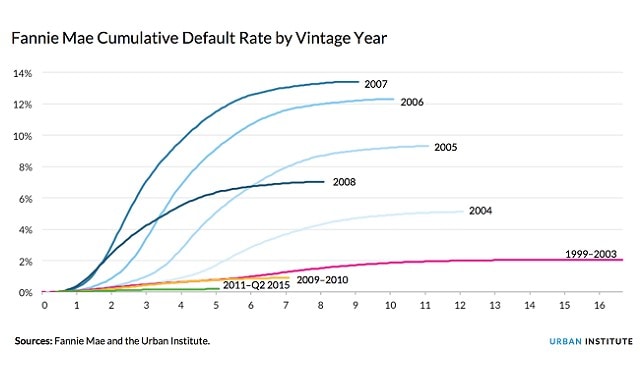

There have been almost no defaults on mortgages originated in the past five years

The default rate on new mortgages is tracking well below mortgages originated from 1999 to 2003, a period with reasonable lending standards and fairly low default rates. This chart illustrates by origination year the rate at which mortgages guaranteed by Fannie Mae have gone six months delinquent (or liquidated before that point). We refer to this as the default rate. The really poor performance of the 2006–08 vintages jumps off the page.

Rest here…

~

From my vantage point , scrubbed clean loans means , not manipulated by a secret contract taking place funded another way with your ” fake Lender ” acting as a servicer of the money streams created by those contract made behind your back and without your permission !!! You have two totally different circumstances happening between 08 and 2016 …..

there are good reason defaults are dow and I am seeing 100% loans and some not so squeaky again. However, I sold a house last week. Price $55,000. Her note even with PMI, taxes and insurance was below $500. She was paying over $700 rent for an apartment so she is sitting pretty.. Her interest rate on FHA was 3.5. We didn’t have that in 2006-2008. We had inflated values, interest rates above 6% or whatever the market would bear, not to mention unscrupulous mortgage brokers who ‘sold;out’ home-buyers for a kick back ARM, interest only loans and piggy back loans with with bubble notes when 100% was available and would have been better. Excuse for high 2nds.. Predatory loans. So yes there are sensible buyers but their alternative is high rent off the charts or live with family! Most buyers now are younger first time buyers with double incomes and little bad history. High-end buyers taking advantage of low rates and their old houses rising up out of their underwater status. Buyers are being careful too, some buying under their limits. My buyer could easily qualify for $90K+ .

\\\\