Mortgage Fraud is a very unpopular topic. It is simply not something anybody wants to talk about at all, let alone trace the corrosive effects of the dishonesty of our neighbors and fellow citizens on the fabric of the economy. However, it is not something that will go away. Indeed, the longer this fundamental problem is ignored or swept under the carpet, the more futile will all economic remedies be to alleviate the weakness and fragility of our financial system.

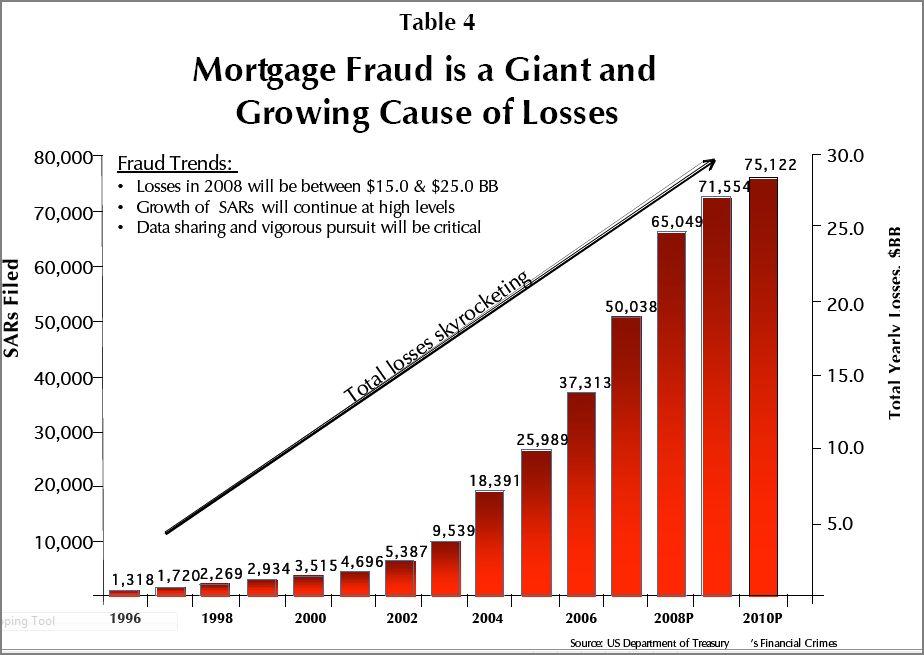

The magnitude of the problem – here is a link (.pdf) to the Eleventh Periodic Mortgage Fraud Case Report, addressed to the Mortgage Bankers Association. According to this document, losses for 2008 will be between 15 and 25 billion. Of course, readers have become inured to big numbers: a billion is now chump change, we need to talk in trillions when addressing the magnitude of our financial woes. That apparent imbalance will be addressed later in this article when discussing the multiplier effect of mortgage fraud.

Insurance Company Evidence – Insurance against mortgage default has been issued in a number of different forms. Mortgage insurance companies, such as MGIC (MTG), Radian (RDN) and PMI (PMI) insure individual mortgages against default, and in addition have done bulk transactions. Financial Guarantors have written insurance, often in the form of CDS, on RMBS and CDOs containing RMBS.

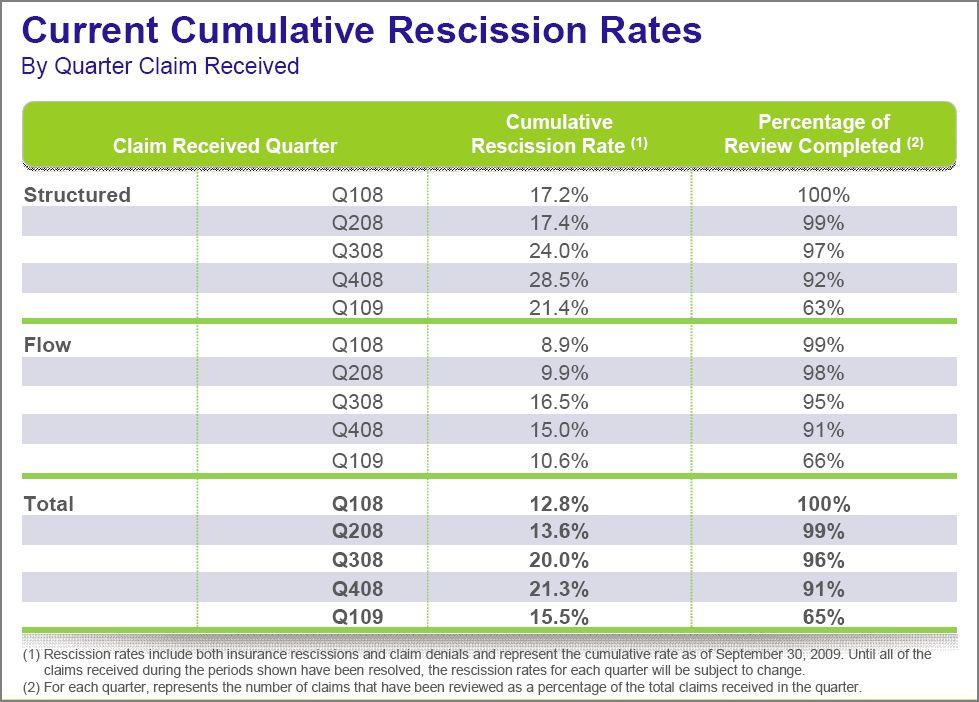

As losses have accumulated, mortgage insurers have investigated the underlying transactions, finding fraud at a rate that I estimate at 15-20% of all insured mortgage loans. They rescind coverage when they find evidence of fraud.

Here is a slide from Radian’s Quarterly Presentation:

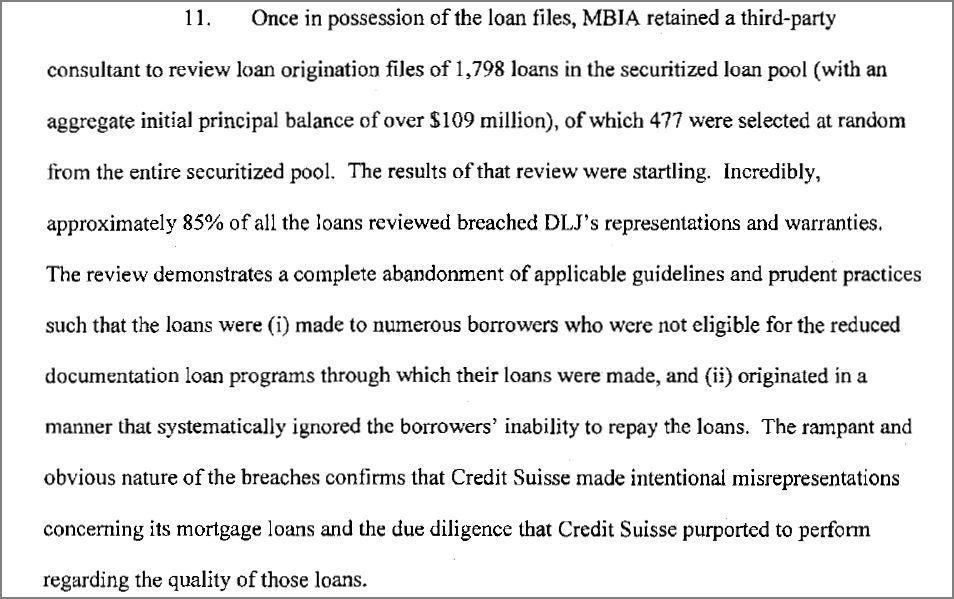

Structured Finance – not surprisingly, the worst of this material found its way into structured finance. Indeed, the apparent ability to pass the inevitable losses on to an endless stream of naïve investors has enabled this trend toward fraudulent transactions to continue far longer than it would have otherwise. MBIA (MBI) insured many of these transactions, and has been active in litigating against fraud. Here is an excerpt from a recent suit against Credit Suisse:

After reading a number of similar complaints, as well as listening to conference calls from MBIA and Ambac (ABK), I form the impression that about 25% of all underlying collateral in private label securitizations was created by fraudulent transactions.

Inadequate interest rates – interest rates around 5% are entirely inadequate to compensate for fraud at a rate somewhere between 15 and 25%. Efforts to restore the housing sector under these conditions are not going to be effective. They will simply compound the problem.

Multiplier Effect – Economists who advocate juicing the economy with fiscal stimulus frequently cite a multiplier effect: every dollar spent by government creates X dollars spent by the private sector. There is a similar multiplier for mortgage fraud: a dollar of mortgage fraud creates many times that amount of loss to the economy.

Property values would never have become so inflated if the spending power fueled by the ability to secure mortgages by fraud had not propelled them upwards. Nor would they have plunged so rapidly if the inevitable foreclosures had not glutted the market with distress sales.

Synthetic securities exacerbated the problem. Not content with creating toxic waste, the investment banks went on to duplicate it, as if by using a photocopy machine to create bogus bonds. Briefly, CDS referencing subprime RMBS were bundled together in synthetic CDOs. CDS are in point of fact insurance transactions, and should be regulated as such, with a requirement of insurable interest on the part of the buyer. Otherwise, problems arise with moral hazard, similar to permitting an arsonist to buy fire insurance on his neighbors house.

Synthetic CDOs in effect were collections of insurance policies that were not backed by insurable interest, and were instead designed and contrived to duplicate losses for the benefit of those who held the CDS protection.

I estimate the multiplier effect at 7X, just like the ratio of the tip of the iceberg to what lies underwater. And mortgage fraud is the iceberg that will sink the Titanic. In point of fact the US economy is listing badly and may still be shipping water.

Futile Fulminations – the American character has become corrupt. The moral backbone of the country has turned to jelly. Anything goes, there is no more right or wrong, the dollar is the only measure of success in life.

Indeed, the meaning of any man’s life lies in his accumulated wealth. Here is a success story: “A man was born. He lied, cheated and stole until he accumulated a fortune. After he died, others enjoyed the fruits of all that he had done. The end.” Here is a story of failure: “A man was born. He didn’t have enough street smarts and the fruits of all his labor were enjoyed by those who lied to him, stole from him, and cheated him. He died in poverty. The end.”

A society that is not built on a foundation of mutual trust has no cohesion: when the ship sinks, it’s every rat for himself.

Pragmatic solutions – Unless we wish to continue to outdo Nigeria as the home of fraudulent enterprise, laws will need to be passed and enforced.

The normal lying that goes with commerce in residential real estate – exaggerating your income so you can buy a bigger house, mis-stating intended occupancy so you can control a house long enough to flip it, filling out the application with answers the applicant would not have given if asked, inflating an appraisal so the transaction can go through, holding your nose while you package the stuff into a bogus bond – will have to be punished by jail time.

It would do something for the economy: those who are jailed can’t hold jobs, making employment available for those who are unconfined and unemployed. Some could become teachers, instructing the public in the consequences of formerly acceptable but now illegal behaviors. Of course, many prisons would need to be constructed. Perhaps they could be designed for dual functionality, the buildings could be used for educational institutions to promote the acquisition of marketable skills in a new world. And prison personnel would be in high demand. Supervising a bunch of white collar criminals would not be anywhere near as dangerous as regular prison work.

Best of all, when mortgage fraud is contained, the multiplier effect will stop destroying wealth.

Source: Seeking Alpha Tom Armistead

4closureFraud

https://4closurefraud.org/

Here is securities fraud and I have every document to prove it.

Now let’a get to the fraud. Mers was named nominee on the mortgage and filed at the Register Of Deeds in Greenville SC, supposedily according to a lost note affidivat the original lender RBMG sold the note and according to MERS servicer ID the loan was transfered off of the MERS system and MIN# deactivated because of a sale to a non-mers member in 2002. NO ASSIGNMENT WAS RECORDED.Now the new owner EMC sold the loan to Bear Stearns which deposited into the Asset Backed Securites which did an assignment/sell to JP MORGAN CHASE as trustee. Now there has been a foreclosure started on the loan in March 2009 by The Bank OF New York Mellon as successor trustee for JP MORGAN CHASE who claims to be the real party in interest and hold the note. By way Of an assignment which was recorded at the ROD after the LIS-PENDENS and after the filing of complaint.Here is more fraud because the assignment was from MERS on behalf of the original lender RBMG which is defunct and has been since 2005 to the THE BANK OF NEW YORK MELLON. MERS has no authority to do an assignment because the loan was transferred from them in 2002 and Mers was Longer the mortgagee as nominee of record.Now are you with me( no chain of title) the BANK OF NEW YORK MELLON produced in discovery to me an allonge RBMG to EMC along with the lost note affidivat. EMC showed an allonge to JP MORGAN CHASE which skipped BEAR STEARNS. BEAR STEARNS was the depositer into the securities. First let start with the allonges: according to the UCC an allonge is only used when there is NO ROOM ON THE ORIGINAL NOTE FOR ENDORSEMENT and must be firmly attached as to become a part of the note. AN ALLONGE cannot be used to transfer interest and is invalid if there is room on the note for endorsements and is invalid it not attached. A lost note and two allonges that were not signed and not dated and even skipped BEAR STEARNS that desposited it into the securities is the purported chain of title , now let’s look at the prospectus:Bear Stearns Asset Backed Securities Inc · 424B5 · Bear Stearns Asset Backed Certificates Series 2003-2 · On 6/30/03

Document 1 of 1 · 424B5 · Prospectus

. Assignment of the Mortgage Loans; Repurchase At the time of issuance of the certificates, the depositor will cause the mortgage loans, together with all principal and interest due with respect to such mortgage loans after the cut-off date to be sold to the trust. The mortgage loans in each of the mortgage loan groups will be identified in a schedule appearing as an exhibit to the pooling and servicing agreement with each mortgage loan group separately identified. Such schedule will include information as to the principal balance of each mortgage loan as of the cut-offdate, as well as information including, among other things, the mortgage rate,the borrower’s monthly payment and the maturity date of each mortgage note. In addition, the depositor will deposit with Wells Fargo Bank Minnesota, National Association, as custodian and agent for the trustee, the following documents with respect to each mortgage loan: (a) except with respect to a MOM loan, the original mortgage note, endorsed without recourse in the following form: “Pay to the order of JPMorgan Chase Bank, as S-40——————————————————————————–

trustee for certificateholders of Bear Stearns Asset Backed Securities, Inc., Asset-Backed Certificates, Series 2003-2 without recourse,” with all intervening endorsements, to the extent available, showing a complete chain of endorsement from the originator to the seller or, if the original mortgage note is unavailable to the depositor, a photocopy thereof, if available, together with a lost note affidavit; (b) the original recorded mortgage or a photocopy thereof, and if the related mortgage loan is a MOM loan, noting the applicable mortgage identification number for that mortgage loan; (c) except with respect to a mortgage loan that is registered on the MERS(R) System, a duly executed assignment of the mortgage to “JPMorgan Chase Bank, as trustee for certificateholders of Bear Stearns Asset Backed Securities, Inc., Asset-Backed Certificates, Series 2003-2, without recourse;” in recordable form, as described in the pooling and servicing agreement; (d) originals or duplicates of all interim recorded assignments of such mortgage, if any and if available to the depositor; (e) the original or duplicate original lender’s title policy or, in the event such original title policy has not been received from the insurer, such original or duplicate original lender’s title policy shall be delivered within one year of the closing date or, in the event such original lender’s title policy is unavailable, a photocopy of such title policy or, in lieu thereof, a current lien search on the related property; and (f) the original or a copy of all available assumption, modification or substitution agreements, if any. In general, assignments of the mortgage loans provided to the custodian on behalf of the trustee will not be recorded in the appropriate public office for real property records, based upon an opinion of counsel to the effect that such recording is not required to protect the trustee’s interests in the mortgage loan against the claim of any subsequent transferee or any successor to or creditor of the depositor or the seller, or as to which the rating agencies advise that the omission to record therein will not affect their ratings of the offered certificates. In connection with the assignment of any mortgage loan that is registered on the MERS(R) System, the depositor will cause the MERS(R) System to indicate that those mortgage loans have been assigned by EMC to the depositor and by the depositor to the trustee by including (or deleting, in the case of repurchased mortgage loans) in the computer files (a) the code in the field which identifies the trustee and (b) the code in the field “Pool Field” which identifies the series of certificates issued. Neither the depositor nor the master servicer will alter these codes (except in the case of a repurchased mortgage loan). A “MOM loan” is any mortgage loan as to which, at origination, Mortgage Electronic Registration Systems, Inc. acts as mortgagee, solely as nominee for the originator of that mortgage loan and its successors and assigns. S-41——————————————————————————–

The custodian on behalf of the trustee will perform a limited review of the mortgage loan documents on or prior to the closing date or in the case of any document permitted to be delivered after the closing date, promptly after the custodian’s receipt of such documents and will hold such documents in trust for the benefit of the holders of the certificates. In addition, the seller will make representations and warranties in the pooling and servicing agreement as of the cut-off date in respect of the mortgage loans. The depositor will file the pooling and servicing agreement containing such representations and warranties with the Securities and Exchange Commission in a report on Form 8-K following the closing date. After the closing date, if any document is found to be missing or defective in any material respect, or if a representation or warranty with respect to any mortgage loan is breached and such breach materially and adversely affects the interests of the holders of the certificates in such mortgage loan, the custodian, on behalf of the trustee, is required to notify the seller in writing. If the seller cannot or does not cure such omission,defect or breach within 90 days of its receipt of notice from the custodian, theseller is required to repurchase the related mortgage loan from the trust fund at a price equal to 100% of the stated principal balance thereof as of the date of repurchase plus accrued and unpaid interest thereon at the mortgage rate to the first day of the month following the month of repurchase. In addition, if the obligation to repurchase the related mortgage loan results from a breach of the seller’s representations regarding predatory lending, the seller will be obligated to pay any resulting costs and damages incurred by the trust. Rather than repurchase the mortgage loan as provided above, the seller may remove such mortgage loan from the trust fund and substitute in its place another mortgage loan of like characteristics; however, such substitution is only permitted within two years after the closing date. With respect to any repurchase or substitution of a mortgage loan that is not in default or as to which a default is not imminent, the trustee must have received a satisfactory opinion of counsel that such repurchase or substitution will not cause the trust fund to lose the status of its REMIC.

I’m not a MOM loan the loan transferred off of MERS, Mers no longer tracked the assignments and let’s not forget I HAVE IN MY POSSESSION THE ORIGINAL NOTE STAMPED FULLY PAID AND SATISFIED NEGOTIATED TO ME FROM RBMG. The note is date stamped MARCH 2002 and has been in my possession since 2004 along with a letter from the RBMG stating the loan is fully paid and satisfied address to me which is the declaritory letter. Come on let’s put these people where they belong…. Federal prison.