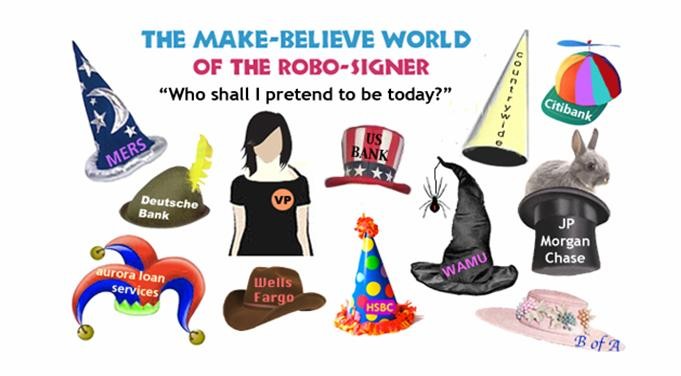

The Dehumanizing Nature of Robo-Signing

Robosigning is criminal, and I’m so grateful that Attorney General Catherine Cortez Masto has the courage and integrity to prosecute people for committing it.

The very term “robo-signing” has, I think, inhibited prosecution because banks have successfully messaged that it was “just a harmless technicality; the real villain is the debtor, he defaulted.” “Just a technicality” is a plausible line because the conjured image is more ridiculous than scary, and as a nation we’re biased against debtors.

We can’t help but be prejudiced against debtors unless we really pay attention, because the anti-debtor public-opinion-shaping/political support-building PR campaign never stops. I mean, it’s been specifically targeted at homeowners since the financial meltdown, but it was used to pass the 2005 Bankruptcy Reform Act which shifted a lot of power from the debtor to the creditor. (Or as the Consumer Federation’s Travis Plunkett put it, ”The bill simply doesn’t balance responsibility between families in debt trouble and the creditors whose practices have contributed to the rise in bankruptcies”.) The anti-debtor campaign was also run during fight over credit card reform, but thanks to a Democratic Congress and a Democratic President, we got the CARD act in 2009. I mean, being anti-debtor has a long American history, including criminalizing default. People were incarcerated in “debtor’s prisons” until New York abolished them in 1831 and other states followed. But I digress.

My point is, robo-signing as a term failed to convey the legal seriousiness of the banks’ and banks’ vendors’ document fraud.

Rest here…

~

This is not the homeowners debt problem…this is Wall Street and the GSE’s debt problem…they caused millions to lose their jobs and businesses in this manufactured mess…..and they all got filthy rich off of it…This was a Hitler Plan and it is about nothing more than stealing all of the wealth and assets from the middle class in the name of debt…not our debt….Wall Street and the GSE’s $600 TRILLLION IN MORTGAGE DERIVATIVES FRAUD DEBT BACKED BY ZERO COLLATERAL…..THEIR DEBT IS UNSTAINABLE AND THERE ARE NOT ENOUGH HOMES AND WEALTH TO STEAL TO PAY FOR ALL OF IT….STOP THE FRAUDCLOSURES AND SEND IN THE FEDS TO AUDIT THE BANKS AND THE GSE’S….THAT IS WHERE THE TRUTH IS….THEY ARE BROKE AND INSOLVENT ON PAPER…THE ROBBERY OF THE AMERICAN PEOPLE TO PAY FOR THE CRIMES OF WALL STREET AND THE GSE’S MUST STOP!!!

You have got to know that Banksters were licking their lips after they bashed consumers over the head in 2005.

Banksters once again stole your consumer protections right out of the law, by paying off your legislators.

Prey on more ‘borrowers”, aka victims, they don’t have a way out now. The 2005 Bankruptcy Reform Act was another attack on you.

Also MERS is criminal. No matter what a journalists says. They have intentionally saved $2.4 Billion because they did not Pay stste and County recording fees. It is jail time and accomplice time as well. Line up.