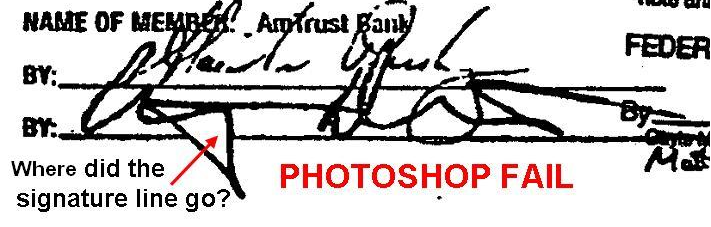

MERS Assignment Fail: Mortgage Electronic Registration Sidesteps, Inc.

Over the years we have seen various Assignment Fails such as BOGUS and BAD BENE. Some even had effective dates as 09/09/9999, while others had forged signatures or were put together by someone with very poor Photoshop skills.

{kind=link}

Today, we present a new variation of a MERS assignment that is polluting land records across the county, the SIDESTEP assignment. Because what could possibly be a better name, other than BOGUS, than SIDESTEP for an industry that has done everything in their power to SIDESTEP hundreds of years of property law to save a couple of bucks.

If you have not caught it yet, reread the name of MERS on this Assignment on the image above or click here…

There must of been an ‘error’ in their SYSTEMS.

Full assignment below…

~

4closureFraud.org

~

MERS Assignment Fail: Mortgage Electronic Registration Sidesteps, Inc.

I’ve been trying to deal with Country-Wide, BOA for almost 10 years. My husband passed in 07,leaving me with a mortgage of $3000. a month, which I couldn’t afford, even though I had an income on the 1st. floor. I’m disabled, widowed and loss my part-time job in 012, when they found out I had Lupus. Every month I sent out all the information the banks requested, informing me that I would be eligible for the new program that had been rolled out by BOA (they bought out Country-Wide) to help borrowers facing foreclosures. This is the Homeownership Retention Program. Well this didn’t happen and I haven’t made a payment since the death of my husband. I’ve had 4 lawyers, (all lairs ) who tell you what you want to hear, when they get your retainer and when things are getting horrible, they denied all the things that were promise to you. This has made me so sick, emotionally and physically that I have 2 nurses & someone to be with me for 21 hours a week, because I can’t function. These banks just keep this paperwork going and waited for the Stature of Limitations ran. I’m 62 years old and I can’t lose my home because I’ll definitely be homeless since I couldn’t live on what Social Security give me! I would appreciated any information anyone could give me.

Is it legitimate if the member-employee to execute the assignment in MERS’ name is an employee of the servicer for the current note holder, i.e.,

the servicer’s boss or principal, who is the transferEE?

Let us focus on the alleged robo-signers who executes the assignments while being under the employment of the transferEE.

Let us all appeal to lawyers giving them confidence that we will all prevail in convincing a state or federal judge to rule against this type of conduct because it is a conflict of interest: MERS, or anyone, should not be authorizing a person connected with, or the agent of, the assignment transferEE to make the assignment in MERS’ name. Not only should this not be allowed – IT SHOULD BE PROHIBITED!!!

MERS should only allow assignments in its name to be done by a person properly associated with the transferOR or at any rate, certainly not someone affiliated with the transferEE. And even then, MERS relationship with the transferor must be identified and the assignment executed accordingly.

This is all the more true because in reality, it’s the transferEE pulling the strings. http://www.sourceoftitle.com/blog_node.aspx?uniq=994

Is it a good defense if we all unite in a Class Action Lawsuit?

Thank you Bobbie!

Thanks Perry. I think you’re right.

Wow!!! What a blast from the 2010 past! – I will NEVER forget the name,

JILL BALLENTINE as long as I live!!!

In OREGON (non- judicial), on my manufactured FRAUD-CLOSURE papers, JILL BALLENTINE’S name was given as the point of CONTACT on The NOTICE OF DEFAULT / NOTICE OF INTENT TO SELL documents mailed from RECONTRUST – (B of A subsidiary)

Those fraud-closure documents were mailed (certified/ registered) at least 13 times to my house & charged to me each time– Jill BALLENTINE’S name was on EVERY one of them. (I STILL HAVE THEM!)

The only problem was that no one knew who she was & the phone number was a fake!

(a B of A phone number that was phoney)

Hell, maybe she was working for

“MER-Sidestep” all along & NOT BofA or ReConTrust (even “Re-Con-Trust” sounds suspicious! Similar to “American Brokers CONDUIT” — both are my players) Boy, did they PLAY us— and sooooo BOLDLY & NON-DISCREETLY

Unbelievable! So obvious in retrospect. So sadly obvious.

Probably intentional to avoid detection in search queries -it looks to also be a ‘global’ replacement “Systems” – “Sidesteps” – still sloppy no matter the intent

They sidestep the law and forge fraud into the court and get away – SIDESTEP PROSECUTION and most times win.

That one is one of the worst I have seen. Who the hxxl is MERS SIDESTEPS????

LDTX How fitting for the Assignment Sidestep, America’s Wholesale Lender, Bank of New York Mellon, and Texas, the state nobody speaks of.

Ocwen used MERS to assign our Deed of Trust (DOT) in foreclosing our home, robo-signed inside a small office of Ocwen in Waterloo, Iowa. This small Ocwen office in Iowa is a foreclosure mill. This fabricated Corporate Assignment of our DOT from Waterloo, Iowa was used by Ocwen and Deutsche to steal a home far, far away from our home in Bothell, Washington about 1,780.4 miles away from them.

On New Year’s Eve December 31, 2014, Brandy Berns, Assistant Secretary of MERS assigned our DOT in favor of Deutsche Bank. This Corporate Assignment of our DOT represented to me and my wife that the new owner of our home’s note is Deutsche, as Trustee for the registered holder of Morgan Stanley Home Equity Loan Trust 2007-2 Mortgage Pass Through Certificates, Series 2007-2. Most probably not securitized or even if it is, our home is not in the prospectus.

Turns out, Brandy Berns is actually an employee of Ocwen. Further, Notary Public Mary Kammeyer, the person that notarized Berns’ assignment of our home, claimed Berns who appeared before her was known to her as Assistant Secretary of MERS – knowing fully well that they are both employees of Ocwen and both are Notary Public with identical Commission numbers issued in the State of Iowa except the last digit. #786692 for Kammeyer and #786691 for Berns. The fact that (on New Year’s Eve, few hours before celebration of the new 2015 year) the notarial executions were placed on a separate page; when there clearly was enough room to generate the executions on the first page is a marker of document manufacturing – which any Examiner construes to mean that the notary did not actually witness the physical signature of the signor to the document. Perhaps they’re too in a hurry because signing hundreds of documents on New Year’s Eve (12/31/2014) was a joy killer.

Although Berns and Kammeyer are both listed robo-signers in more than 1 independent website, Ocwen produced a MERS document authorizing both to assign DOTs. I can provide a copy of the list of names allegedly authorized by MERS to anyone who might need this list for comparison to defend their home.

However, being in Washington State, in the foreclosure sale case of Hooker V. B of A Wells QLS shows void ab initio because the “substituted” trustee never had the authority to send the notice of default nor the notice of sale especially in a non-judicial state like the State of Washington. This case further warns Ocwen Loan Servicing (Ocwen) that our home’s Foreclosure Sale violated 2 of the Washington Deeds of Trust Act with the non-judicial foreclosure of our Deed of Trust:

(a) a violation RCW 61.24.010(1)(a), which requires a corporate Trustee to have at least one corporate officer who is a Washington resident; and/or

(b) a violation RCW 61.24.010(2), which requires a Trustee of a deed of trust to have been appointed by the beneficiary of the deed of trust.

I hope I have a case that a lawyer out there is interested or can refer me to your lawyer friend in Washington State.

Thanks all,

Virgil

Oh I do hope you find representation. You have such a good case. I especially love how when a mortgage is placed in a MBS it actually becomes a percentage of the whole and to actually foreclose you woul dhave to substitute that percentage with another pledged asset (mortgage) to take it’s place. Those MDS’s are sold with guarantees of returns and when you deplete the asset by removing a mortgage to foreclose, you have to replace it or the entire MBS files the foreclosure and we all know that that cannot happen. Good Luck but know that good defense foreclosure attorneys are not cheap.

and hope that you can find a honest lawyer. Most are born liars. looking back, the only thing a lawyer did was buy you a little time for the inevitable

Virgil, you sure did your homework !!! I KNOW what you are going through– I’m in Oregon & similar thing happened to me in 2010- I’m self-educated on the subject as well. Fortunately, for me, I was able to save our house the same week as the sheriff’s sale — however, it now feels like it was UNFORTUNATE because, SEVEN years later, I’m still dealing with this shit & tired of having this albatross of a house hanging around my neck & dictating my life.

We NEED to sell & move out of state but the 2nd has “disappeared” (Ocwen), but there’s still a lien on the house & our first (SHELLPOINT Mortgage Servicing) obviously does not have our deed or note because they are not following the terms of the note — they’ve been billing us incorrectly for 18 mos (in our favor) & we believe they are a made up LLC that is just pocketing our monthy mortgage payment.

Would YOU want to buy our house ??!! Title issues ??

What do we REALLY owe ? WHO do we pay when we do find a buyer?

Many times a wish we were still upside down so I’d feel I could just walk. It would be so much easier.

Best of luck to you– get on livinglies.org website & look under the tab, “lawyers that get it”— there’s a few listed in every state. I recall WA being pretty proactive in going after some of these banksters.

You can google WA state cases & see who some of the prosecuting law firms & lawyers are. I remember there was one in Seattle that did a class action — against BofA , Recontrust & they won

Also, didn’t Washington just hit OCWEN hard last month? Regarding licensing issues or something? Anyway, good state to be in!

Krista – Oregon is a Deed of Trust state as opposed to a mortgage state. In all cases, the actual Deed to your property is NEVER held by the lender. YOU are given the Deed once it has been recorded of record from the sale between the buyer and seller. The Deed of Trust (in your state) is the instrument by which the lender secures the property as repayment of the Promissory Note. It sounds like it was your second mortgage (Ocwen) who initiated a foreclosure and you were able to get that extinguished? I can tell you that Shellpoint is related to New Penn Financial and was also known as Resurgent back in 2013. Al you have to do is write a letter called a Qualified Written Request detailing that you are requesting ‘certified’ copies of your Deed of Trust, Note and any other documents you want. Be sure to send this with return receipt as they (Shellpoint) have to respond within 30 days of their receipt. I would then also contact the provider of your Title Insurance Policy if you feel that there is a break in the chain of title and file a claim. If nothing else ask them to run a title search (usually a cost of $75) on your property.

Thanks Krista.

How much did you advertise your house price for?

GIVE UP THE LAWYER IDEA, REPRESENT YOUR SELF ! NO LAWYER WILL TAKE YOUR CASE, THEY’LL TAKE YOUR MONEY . THE COURTS ARE RIGGED AND

RUN BY THE CORPORATE WHORES WHO ARE ” FREE MASONS ” !! I KNOW THIS

BECAUSE I RAN THE GAUNTLET OF THE COURTS AN GOT SCREWED BY BOTH

THE STATE AN FEDERAL COURTS !! ONLY THE ” FREE MASONS ” COULD PULL

OFF A SCAM SUCH AS !!! THE NEW WORLD ORDER IS SHOWING IT’S FACE !!

MY MORGAGE WITH BANK OF AMERICA WAS NOTHING BUT FRAUD, JUST AS

YOUR’S IS !

GO TO COURT WITH YOUR CASE, WIN YOUR OWN RESPECT AN SAVE YOUR

MENTALLY !

RICHARD PERRY PRATT

Sorry Richard Perry Pratt but where’s your proof of your statements made? The courts are run by the Freemasons? Only the Freemasons could pull off a scam such as…what? And you are connecting the Freemasons with the NWO? If you ‘ran the gauntlet’ means that you were punished for defending yourself? Granted, and I agree that the courts are corrupt but my personal opinion is that it is born out of power and greed (money). This poor man will drown himself as Pro Se and all Plaintiff attorneys know that and count on it when a Pro Se defendant appears in court. Instead of making accusations (which probably can’t be documented with proof) the people of this country need to be awakened and begin to exercise their right to vote but vote KNOWING the person running for Judge. And IF you honestly believe in the statements you made then understand that the majority of Freemasons are Democrats, and if you are one as well, then YOU are as much to blame for the corruption as to whom you have accused.

What a phucking joke!!

Hi Bobbi

Thanks for your reply. Did this happen to you or do you work in the industry?

To clarify your post, here are some of the details of what happened in 2010… if you’re interested:

It was our 1st mortgage servicer (BofA at the time) that initiated foreclosure, not Ocwen (2nd) – I got the fraud-closure stopped the week of the sherrif’s sale & BofA/ BAC servicing/ Recontrust- (the assigned “beneficiary” who initiated foreclosure & conveniently, a subsidiary of BofA) filed a rescinded notice of default with the county. They ACTUALLY cashed the $15,000 I sent, registered mail, to reinstate my loan (THAT was the problem, they would not accept my monthly payments – assholes- and initiated foreclosure! I’ve only home for 20 years now).

My house was upside down in 2010, so Ocwen (2nd) gave up on the idea of collecting while in pre- foreclosure & went off the radar for years- they stopped billing us. With some research, I discovered that Ocwen closed the account in 2011 & passed/sold? the 2nd mortgage onto their debt collector subsidiary, NCI (there’s a contact in India assigned to our account!). They’ve never billed us properly, just occasionally we’d get a “pay $30k today & we’ll remove your lien!” type of shit. Haven’t made a payment to Ocwen /NCI in over SEVEN years, so I believe the statute of limitations is up- 6 years for written in OR (recently, I read on the FTC website that if a debt collector/ servicer obtained rights to a mortgage during default, it falls under Federal FDC Laws & are treated like a regular ol’ debt collector (I’m looking into this now because I HAVE to get the lien removed)

Yes, there have been breaks in the chain of title, assignments not made, fraudulent, Robo-signed documents with the same name being used on several different documents- all recorded at the county records office. (“Christina Balladran” is one of the “Burger King” kids/ robo-signors from Simi Valley, CA area).

SHELLPOINT (1st) is the tricky one- I’ve paid on my loan since 2005 & I’m current & always have been, with the exception of 4 mos when BofA manufactured & attempted their fraudulent foreclosure in 2010—

SHELLPOINT is completely messing up our billing, they obviously do not have our deed or note because the do not know the terms of our note. The “lender” of my 1st note (2005) is the shell company, American Brokers Conduit – a nonexistent company which NEVER did exist- just a DBA. My servicer in 2005-2007 was American Home Mortgage servicer– went bankrupt around 2007??? then, my servicer became BofA. THEN, BofA used the name BAC Servicing JUST during fraudclosure– went back to BofA Servicing right after they rescinded the fraudclosure, then BofA transferred servicing to “Resurgent”, then Resurgent changed their name to SHELLPOINT. (Hmmmm, wonder why the name change?)

So, here we are today, seven years later. We need to sell & move SOON! Been here 20 years.

I will do the QWR, but would rather have a lawyer write it up.

I am curious about your comment about my title insurance covering or paying for a break in the chain of title. Where were you going with that? I have run title reports within the last year & have it.

My big concern is that I don’t trust that SHELLPOINT will release the lien when I sell my home. Also, I don’t think SHELLPOINT can legitimately calculate a payoff balance, nor do I trust where the money would go since my lender did not actually exist and I’m about 100% sure the MBS/ trust pool does not exist. If it does, my loan is not on it..

I think it may be AHM AssetsTrust

2005-1

I’m thinking of taking advantage of the freedom of info act recently passed that applies to Freddie Mac — FREDDIE supposedly owns my 1st loan !

https://livinglies.wordpress.com/2017/05/02/h-r-1694-passes-fannie-and-freddie-open-records-act-of-2017/

Anyway, any help/ comments are welcome & appreciated.

Few days ago, South Carolina joined 2 dozens of other States file a flurry of similarly worded legal actions to block Ocwen.

On the same day that the Consumer Financial Protection Bureau (CFPB) filed suit, South Carolina joined 24 other states in issuing cease and desist orders against Ocwen Loan Servicing, LLC, a Florida-based corporation with headquarters in Delaware and the U.S. Virgin Islands. The CFPB accused Ocwen of “years of widespread errors, shortcuts, and runarounds,” costing some borrowers money and other borrowers their homes.

“The main concern we have is Ocwen’s failure to reconcile its escrow accounts,” said Carri Grube Lybarker, administrator of Consumer Affairs. In some cases, she added, the firm “was unable to show money going in was being credited” to the borrowers.

South Carolina issues cease and desist order against large mortgage servicer facing CFPB charges.

The nations’ second largest non-bank mortgage servicer, servicing 1.5 million families, violated several state and federal laws, South Carolina and federal regulators find.

CFPB is a valuable partner to states and helps them protect consumers from financial abuses,” said Lauren Saunders, associate director of the National Consumer Law Center. “Any attempt to weaken the CFPB leaves families in South Carolina and across the nation vulnerable to violations of their rights.”

“People have no choice of the mortgage servicer that handles their loan, and yet the servicer’s misconduct can cause families to lose their homes. That is why vigilance by the CFPB and state regulators is so important to send a message to financial service providers that misconduct will not go unpunished,” Saunders added.